Sun Belt Housing Crash: Buyers Are Now Purchasing Homes 25–40% Below Peak Prices in 2026

July 14, 2026

July 14, 2026

The Sun Belt Housing Crash is no longer just a forecast.

It’s becoming a reality in several of America’s hottest pandemic-era housing markets. Buyers who were priced out just a few years ago are now purchasing homes at discounts of 25% to 40% below peak prices, a dramatic reversal from the bidding wars that defined the 2020–2022 housing boom.

One recent example highlights just how quickly conditions have changed.

A home purchased near the market peak in 2021 recently sold for 25% less, wiping out years of appreciation in just a few transactions.

Similar price cuts are becoming more common across parts of Florida, Texas, Arizona, and other Sun Belt markets where inventory has surged and buyer demand has cooled.

The latest data from the Reventure App shows this isn’t an isolated trend. Rising inventory, slowing migration, and worsening affordability have shifted negotiating power firmly toward buyers in many Sun Belt metros.

Sellers who expected pandemic-level prices are increasingly being forced to accept significant discounts to close deals.

These market conditions reinforce concerns we explored in our analysis of the U.S. housing bubble, where rapidly rising inventory and weakening affordability pointed to growing downside risks in several formerly high-growth markets.

Housing Inventory Growth Across Major Sun Belt Markets (2026 vs. 2022)

| Metro | Inventory Growth |

|---|---|

| Austin | +68% |

| Tampa | +61% |

| Phoenix | +55% |

| Nashville | +49% |

| Dallas | +38% |

| Orlando | +36% |

The Sun Belt Housing Crash Is Accelerating

The housing boom that transformed the Sun Belt during the pandemic is losing momentum.

Markets that once experienced double-digit annual appreciation are now dealing with rising inventory, longer selling times, and growing numbers of price reductions.

Buyers have more choices than they have had in years, creating a very different market from the one that existed just three years ago.

Several factors are driving the slowdown. Mortgage rates remain elevated, making homeownership less affordable than during the pandemic.

At the same time, builders have delivered thousands of new homes, increasing supply just as buyer demand has weakened. The result is a market where sellers are competing harder for fewer qualified buyers.

This shift has been especially noticeable in markets that experienced the fastest price growth during the pandemic.

Cities that once saw homes receive multiple offers within days are now seeing listings remain on the market for weeks or even months. That increase in inventory is giving buyers far greater negotiating leverage.

Why Buyers Are Paying Well Below Peak Prices

The biggest reason behind the Sun Belt Housing Crash is the growing imbalance between supply and demand. Even major forecasters have become more cautious as inventory continues to rise.

Zillow’s updated housing market forecast now reflects a much softer outlook than earlier projections, highlighting how quickly market conditions have changed.

During the pandemic, migration into states like Florida, Texas, and Arizona pushed housing demand to record highs. Builders responded by accelerating construction, expecting population growth to continue indefinitely.

Today’s market looks very different. Migration into many Sun Belt cities has slowed while new homes continue entering the market.

Existing homeowners are also listing properties at a faster pace, creating even more competition among sellers. That combination has made it much easier for buyers to negotiate lower prices.

The Market Is Returning to Normal

It’s important to distinguish today’s Sun Belt Housing Crash from the 2008 housing collapse. Lending standards remain significantly stronger, and most homeowners still have substantial equity.

Instead of widespread foreclosures, today’s price declines are being driven primarily by affordability challenges and rising inventory.

That distinction matters because it suggests the correction is being led by market fundamentals rather than financial distress.

Home prices rose much faster than incomes during the pandemic, creating affordability problems that eventually reduced buyer demand. As supply increases and demand cools, prices naturally begin adjusting toward more sustainable levels.

Where the Biggest Discounts Are Appearing

The Sun Belt Housing Crash isn’t affecting every market equally. The deepest discounts are appearing in cities that experienced the largest pandemic price gains and the biggest increases in housing supply.

In several vacation-driven Sun Belt markets, the slowdown is also being amplified by weakening short-term rental demand.

As we explained in our article on Airbnb’s impact on the housing market, more investors are listing properties for sale as rental income softens.

Many of these markets are concentrated across Florida, Texas, Arizona, and parts of the Mountain West, where builders dramatically expanded construction between 2020 and 2023.

The correction is also creating opportunities for buyers willing to negotiate. Homes that would have attracted multiple offers during the pandemic are now selling after several price cuts.

In some cases, sellers are accepting offers 25% to 40% below their peak market values, particularly when properties have remained unsold for several months.

Why Sellers Are Accepting Bigger Losses

Many homeowners entered the market near the peak of the housing boom. They expected prices to continue climbing and listed their homes based on outdated market conditions.

As inventory continued increasing, however, many discovered that buyers were no longer willing to pay pandemic-level prices.

Higher mortgage rates have reduced purchasing power for nearly every buyer. A home that seemed affordable at a 3% mortgage rate often becomes unaffordable at rates above 6%.

Sellers who need to move are increasingly lowering prices rather than waiting for demand to recover.

The data shows these price corrections aren’t just theoretical; they’re already happening in many Sun Belt markets.

In the video below, I walk through real-world examples of buyers purchasing homes at 25% to 40% below peak prices, explain why more distressed sellers are accepting steep discounts, and outline the market conditions that are creating these opportunities.

Price corrections don’t happen because sellers suddenly want to accept less money. They occur because changes in affordability affect buyer behavior.

As mortgage payments climbed over the past several years, demand weakened while inventory continued to grow.

Why the Sun Belt Housing Crash Is Accelerating

| Year | Mortgage Rate | Active Inventory Index |

|---|---|---|

| 2021 | 3.0% | 100 |

| 2022 | 5.3% | 112 |

| 2023 | 6.8% | 136 |

| 2024 | 6.9% | 149 |

| 2025 | 6.5% | 162 |

| 2026 | 6.6% | 171 |

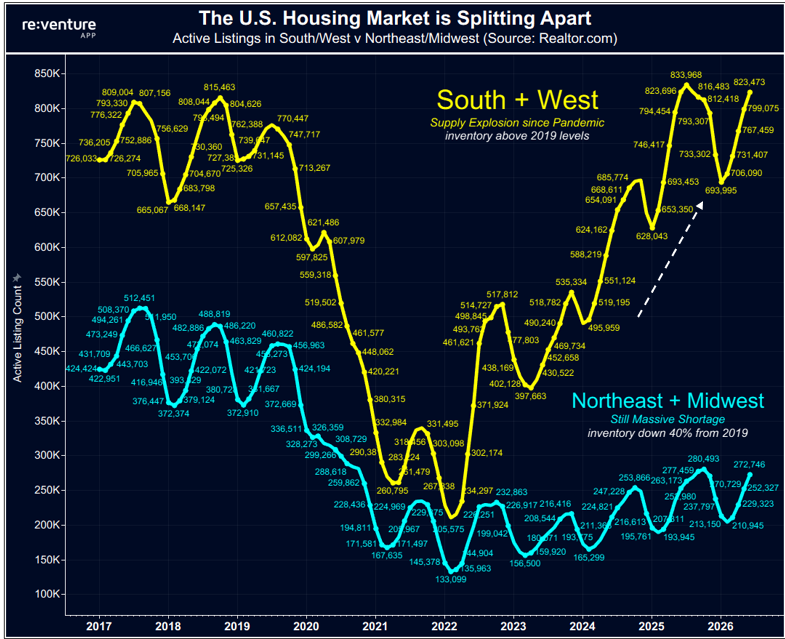

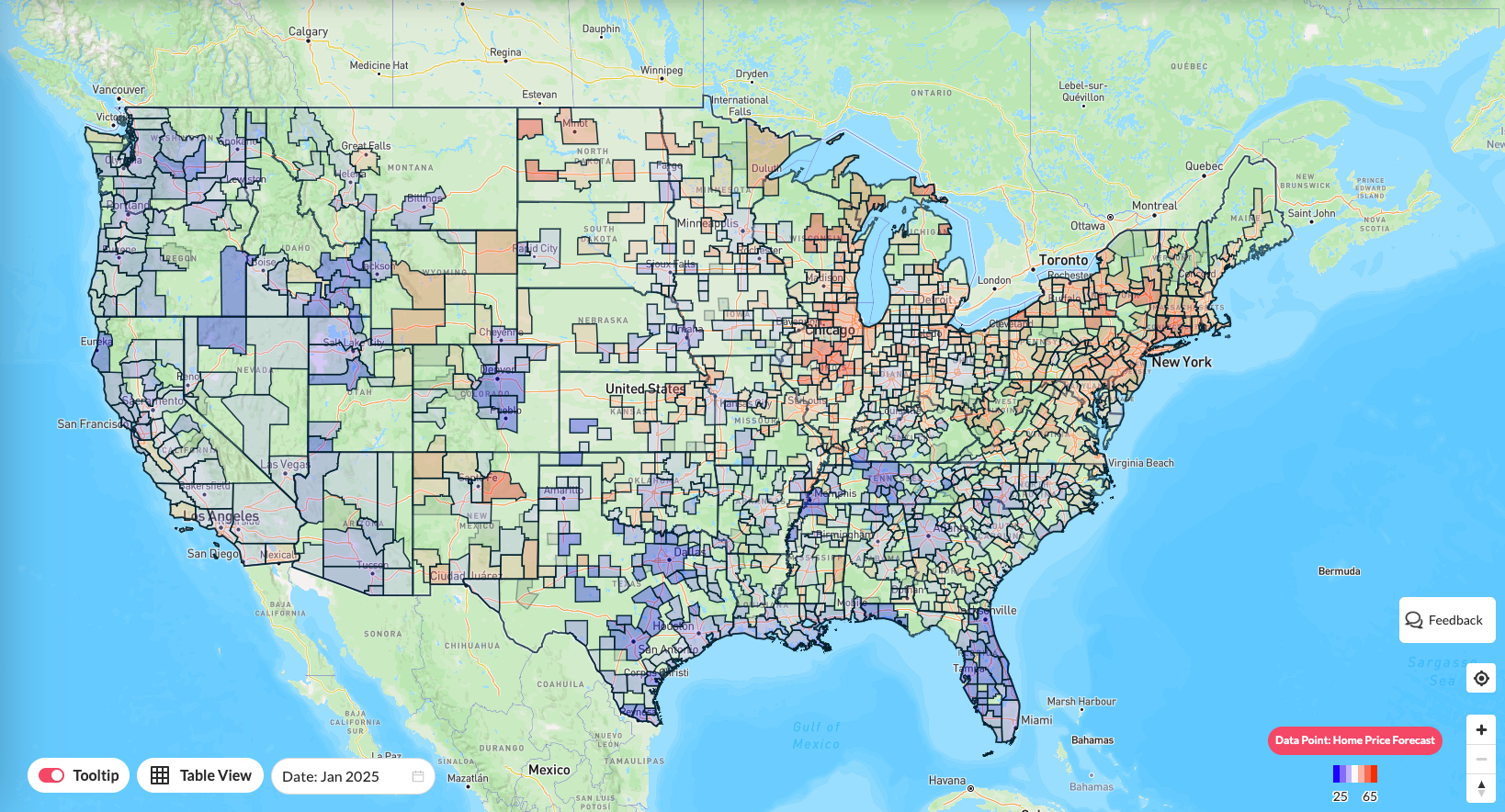

The Midwest and Northeast Are Telling a Different Story

While the Sun Belt Housing Crash gains momentum, many markets across the Midwest and Northeast continue showing much stronger fundamentals.

Inventory remains relatively limited in several of these regions, preventing the sharp price corrections now occurring across parts of the South.

That growing regional divide highlights an important shift in the U.S. housing market. During the pandemic, nearly every major market experienced rapid appreciation.

Today, housing performance depends much more on local inventory, affordability, and migration trends than on broad national conditions.

What the Sun Belt Housing Crash Means for Buyers

For buyers, today’s market presents opportunities that haven’t existed in years. More inventory means more choices, less competition, and greater negotiating power.

Patient buyers may be able to secure meaningful discounts, especially on homes that have been listed for an extended period.

At the same time, buyers should remain selective. Not every Sun Belt market is correcting at the same pace, and some neighborhoods continue outperforming others.

For investors, falling home prices are only one part of the equation. Rental yields and cash flow remain just as important, which is why our guide to the highest cap rate markets in America. Local housing data is becoming far more valuable than national headlines when deciding where and when to buy.

What Happens Next in the Sun Belt Housing Crash?

The Sun Belt Housing Crash is ultimately a story of supply catching up with demand. Years of rapid homebuilding, slowing migration, and weaker affordability have shifted many formerly red-hot markets from severe shortages to growing inventory surpluses.

Until that excess supply is absorbed, sellers are likely to remain under pressure, giving buyers more opportunities to negotiate.

That’s why local housing data has become far more valuable than national headlines.

The Reventure App lets you track inventory, home prices, days on market, and neighborhood-level trends for your ZIP code. Whether you’re buying, selling, or investing, local data can help you identify opportunities before they become obvious to the broader market.

Explore your local housing market today with the Reventure App and see where prices, inventory, and demand are heading in 2027.

Frequently Asked Questions

1. Is the Sun Belt housing market crashing?

The Sun Belt housing crash is affecting several markets where inventory has risen sharply, and buyer demand has weakened. While not every city is declining, many metros are seeing larger price cuts and longer selling times.

2. Why are home prices falling in the Sun Belt?

Home prices are falling because housing supply has increased while demand has slowed. Higher mortgage rates, weaker migration, and more homes for sale have shifted negotiating power toward buyers.

3. Which Sun Belt housing markets are seeing the biggest price declines?

Some of the largest price corrections are occurring in parts of Florida, Texas, Arizona, and Nevada, where inventory has climbed well above pre-pandemic levels. Local market conditions vary, making ZIP code-level data essential.

4. Is 2026 a good time to buy a home in the Sun Belt?

For many buyers, 2026 offers better opportunities than the past few years. Rising inventory, more price reductions, and builder incentives have made it easier to negotiate favorable deals in many Sun Belt markets.

5. Will the Sun Belt housing crash continue into 2027?

The outlook depends largely on inventory, mortgage rates, and buyer demand. If supply continues to outpace demand, the Sun Belt housing crash could extend into 2027, particularly in markets with significant overbuilding.