Why aren’t Americans buying houses?

It’s simple: mortgage Affordability. Buying a home has become significantly more expensive than it was just a few years ago. Today, the typical American household spends approximately 38% of its income on mortgage payments, placing mortgage costs near one of the highest stress levels seen in decades.

As home prices and borrowing costs have increased faster than wages, millions of prospective buyers have found themselves priced out of the market despite still wanting to own a home.

This affordability challenge has persisted since the housing boom of 2021 and 2022. The result is a housing market where demand remains constrained not because buyers have disappeared, but because affordability has deteriorated faster than incomes have grown.

Mortgage Affordability Has Become the Housing Market’s Biggest Challenge

Housing markets are driven by many factors, including inventory, employment, migration, and interest rates. However, none of those factors matter if buyers simply cannot afford the monthly payment.

Mortgage affordability has become the primary force shaping today’s housing market because it directly determines how many households can realistically purchase a home.

One of the best ways to measure affordability is the mortgage-to-income ratio, which compares the typical monthly mortgage payment with household income. Historically, this metric has provided a reliable indication of when housing demand strengthens or weakens.

Home Prices and Mortgage Rates Rose Faster Than Household Income

The affordability problem facing today’s buyers did not develop because of one event alone. It emerged from the combination of rapidly rising home prices during the pandemic housing boom and sharply higher mortgage rates that followed.

While wages increased during the same period, income growth simply failed to keep pace with the rising cost of financing a home.

For many households, the monthly payment has become the deciding factor.

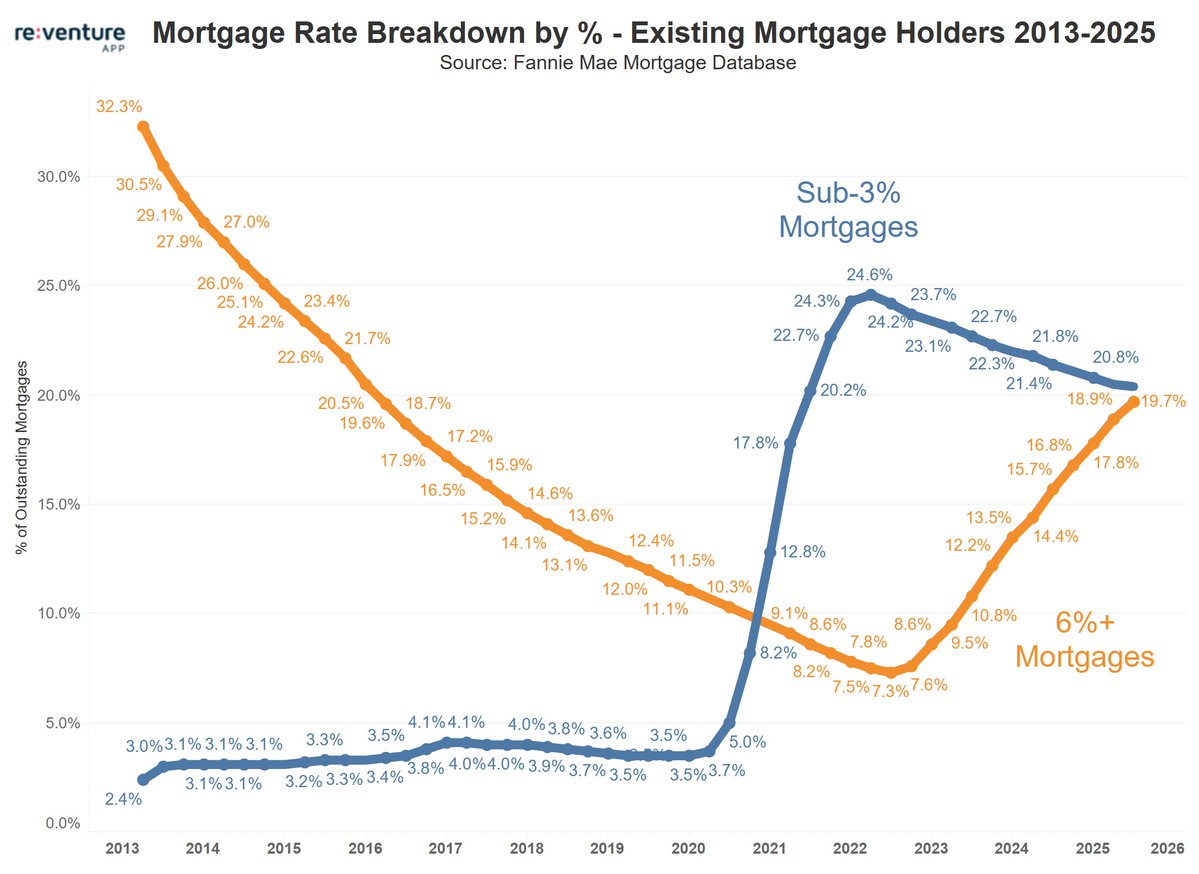

Even buyers who earn more today than they did four years ago often discover they can afford less house because higher interest rates have significantly increased borrowing costs. That reduction in purchasing power is now visible across much of the country.

Why Monthly Payments Matter More Than Purchase Price

Many buyers focus primarily on listing prices, but monthly affordability ultimately determines whether a purchase is financially realistic.

Mortgage interest, property taxes, homeowners insurance, and, in some markets, HOA fees all contribute to the total monthly housing expense. When financing costs rise, even modestly, the payment can increase far faster than buyers expect.

This is one reason online searches for “how much mortgage can I afford“ have become increasingly popular. Prospective homeowners are trying to understand what fits comfortably within their budget rather than simply calculating the maximum amount a lender will approve. In today’s market, those two numbers are often very different.

Today’s Buyers Are Taking on Record Levels of Debt

Most households simply cannot afford to buy a home in today’s market, helping explain why buyer demand remains historically weak.

Meanwhile, buyers who are still purchasing homes are taking on record levels of debt, with Fannie Mae reporting an average back-end debt-to-income (DTI) ratio of 39.6% for new mortgages in 2025, the highest on record and above the 38.7% peak during the 2007 housing bubble.

Rather than affordability improving, many buyers are qualifying only by stretching their budgets further than ever before.

Determining Mortgage Affordability in Today’s Market

For prospective buyers, affordability is about more than qualifying for a loan. It is about understanding whether monthly housing costs can be sustained comfortably over the long term and how conditions vary from one market to another.

That’s why determining mortgage affordability requires evaluating both your finances and local housing data. It is something you can do with the Reventure App, because it tracks affordability, home prices, and mortgage payment trends for every ZIP code in the U.S.

Lenders typically consider household income, debt obligations, credit history, down payment, and prevailing mortgage rates when calculating borrowing capacity. While these factors determine what buyers may qualify for, they don’t always reflect what feels financially comfortable after accounting for everyday living expenses.

Why This Housing Cycle Is Different From Previous Downturns

The current affordability crisis shares many similarities with previous housing cycles, but it also has one important difference.

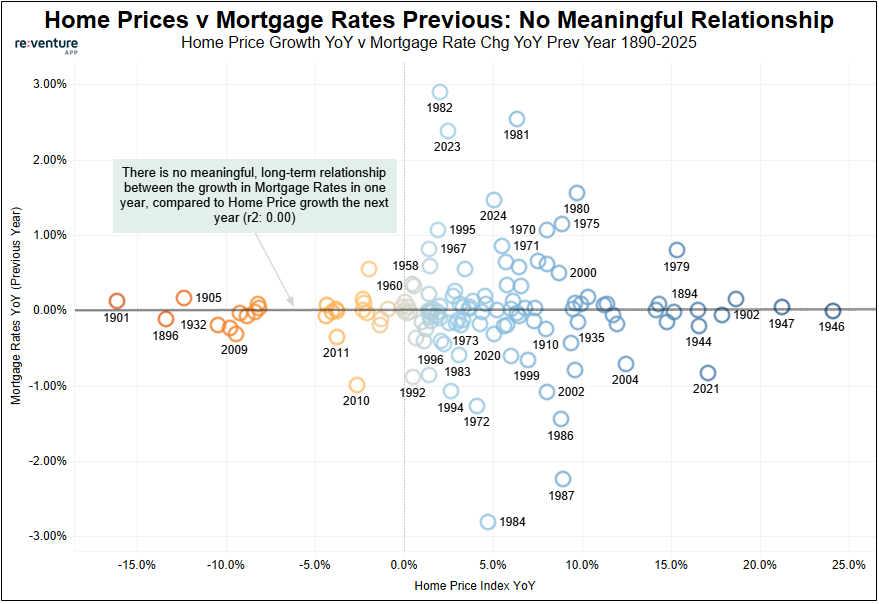

During the 2006 housing bubble and several regional housing booms in the late 1980s, affordability eventually improved through a combination of lower home prices, falling mortgage rates, and rising household incomes. Together, those factors reduced monthly housing costs and encouraged buyers to return to the market.

This time, the outlook appears different. Mortgage rates are unlikely to return to the historically low levels seen during the pandemic, meaning borrowing costs may remain structurally higher. If that happens, restoring mortgage affordability will depend far more on home prices and household incomes than on lower interest rates alone.

Home Prices Are the Biggest Affordability Problem

While mortgage rates receive much of the attention, history suggests they are only part of the story.

Looking back more than 130 years, inflation-adjusted U.S. home prices have never been higher, sitting roughly 80% above their long-term average, while mortgage rates remain only slightly above their historical norm.

That imbalance suggests restoring affordability will depend more on how home prices and incomes adjust than on waiting for significantly lower interest rates.

What Would It Take to Restore Housing Affordability?

Restoring affordability doesn’t necessarily require a housing crash or dramatically lower interest rates.

Based on Reventure’s Mortgage Cost Matrix, the fastest path back to a 30% mortgage payment-to-income ratio would be a combination of roughly a 15% decline in home prices and mortgage rates returning to their long-term average of about 5.6%.

That combination would significantly reduce monthly housing costs and help restore affordability to historical norms.

Of course, housing markets rarely adjust in a straight line. Prices, mortgage rates, and household incomes all move independently, meaning affordability could improve through several different combinations of slower price growth, wage gains, or lower financing costs. But the matrix highlights one important point: home prices remain the biggest variable driving today’s affordability challenge.

Frequently Asked Questions

1. How much mortgage can I afford?

The amount you can afford depends on your income, existing debt, down payment, interest rate, and local housing costs. Keeping your mortgage payment near 30% of your gross monthly income is generally considered a sustainable benchmark.

2. What is mortgage affordability?

Mortgage affordability refers to how comfortably you can manage monthly mortgage payments based on your income and financial obligations.

3. Should I use a mortgage affordability calculator?

Yes. A mortgage affordability calculator is a helpful starting point for estimating your monthly payments, but you should also factor in property taxes, homeowners insurance, maintenance costs, and local market conditions before buying.

4. How is mortgage affordability determined?

Determining mortgage affordability involves evaluating your household income, debt-to-income ratio, down payment, mortgage interest rate, and ongoing housing expenses. These factors help estimate whether a home fits comfortably within your budget.

5. Why is mortgage affordability so low right now?

Mortgage affordability has declined because home prices and mortgage rates have risen much faster than household incomes. As a result, today’s typical buyer spends a much larger share of their income on housing than historical averages, reducing overall buyer demand.

Should Buyers Wait for Affordability to Improve?

Not everyone believes affordability will return to historical norms anytime soon. In a June 2026 report, Morgan Stanley suggested that buyers shouldn’t necessarily wait for mortgage affordability to fully recover, arguing that limited inventory and structurally higher housing costs could keep the market more expensive than many expect.

Whether that outlook proves correct remains uncertain. History shows housing affordability has eventually improved after previous periods of extreme stress, but the path has differed from one cycle to another. The bigger question isn’t whether affordability improves; it’s how it improves, and how long that process takes.

Affordability Will Determine What Happens Next

The biggest challenge facing today’s housing market isn’t a lack of buyer interest. It’s mortgage affordability. As long as home prices and borrowing costs continue to outpace income growth, many buyers will remain on the sidelines, limiting demand and slowing the pace of the market.

History suggests that housing becomes much more active when mortgage payments move closer to 30% of household income. Whether that happens through slower home price growth, stronger wage gains, or a combination of both, affordability will remain the single most important metric to watch over the next several years.

That’s exactly why we built the Reventure App. You can track mortgage affordability, monthly payment estimates, home prices, and local housing trends for your ZIP code in real time, giving you a clearer picture of where affordability is improving and where market conditions remain stretched.

If you want to understand where the housing market is headed next, start with the data.

Explore your local market today with the Reventure App.