Wall Street has stopped buying houses.

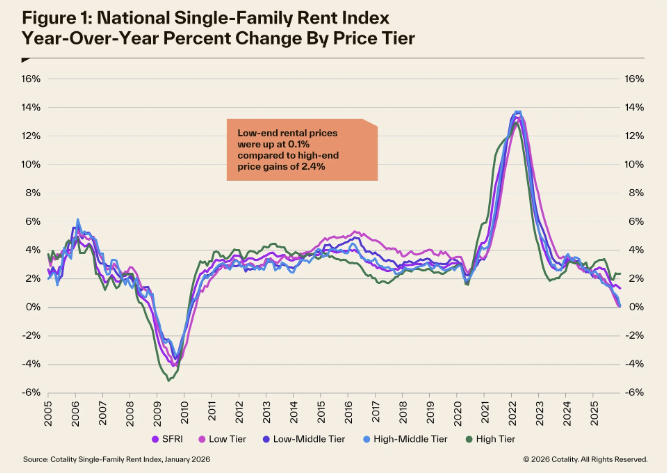

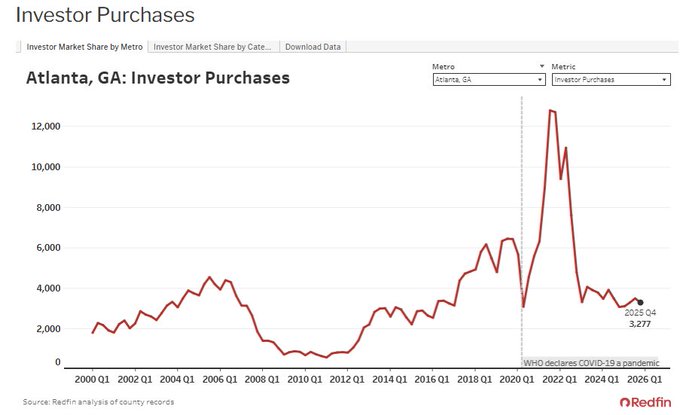

In some of the biggest investor-heavy markets like Atlanta, investor purchases are now down roughly 70% from their peak, falling to the lowest levels in a decade. At the same time, rent growth across the U.S. has slowed to its weakest level in over 15 years, according to CoreLogic data.

Those two shifts are happening simultaneously, and they are starting to change the direction of home prices.

The financial incentives that drove billions of dollars into housing have disappeared, while the income investors rely on is no longer growing. In many markets, both sides of the equation are now deteriorating at the same time, creating real downside pressure on prices, especially in investor-heavy metros across the Sunbelt.

That shift also raises a bigger question. When will it actually be a good time to buy?

Because as Wall Street pulls back, the market is beginning to transition away from institutional dominance and back toward smaller investors and everyday buyers. The same buyers who were previously crowded out may soon have more negotiating power as supply rises and competition fades.

This means we could be witnessing the end of the corporate investor era in U.S. housing, even if recent proposals to ban investor purchases never pass.

The Fed Engineered the Investor Housing Boom

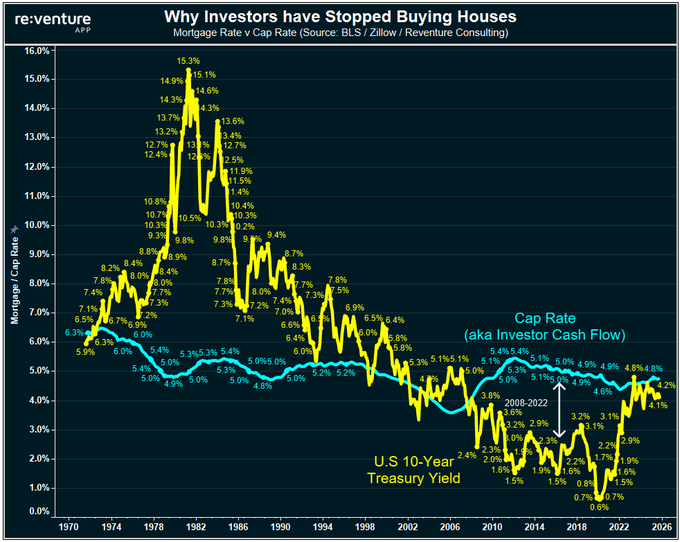

To understand what is happening now, you have to go back to 2008. In the aftermath of the financial crisis, the Federal Reserve launched one of the most aggressive monetary easing cycles in U.S. history. Through quantitative easing and zero interest rate policy, the Fed suppressed long-term yields for more than a decade, keeping the 10-year Treasury yield largely in the 1 to 3 percent range.

At the same time, housing cap rates, which represent the return investors earn from rental income, remained relatively stable between roughly 4 and 6 percent. That created a persistent spread where buying homes and renting them out generated higher returns than holding government bonds. For institutional capital, that spread was highly attractive.

This dynamic transformed housing into a yield-driven asset class. Wall Street firms, private equity, and large-scale landlords deployed billions into single-family homes, scaling portfolios across markets like Atlanta, Phoenix, Tampa, and Las Vegas. What followed was the largest investor-driven housing expansion in U.S. history, supported not by fundamentals alone, but by artificially low interest rates that made the trade work.

That Financial Advantage Has Now Disappeared

That entire equation has now flipped. Over the last two years, the 10-year Treasury yield has surged back into the 4 to 5 percent range, effectively eliminating the spread that made housing so attractive to investors. In many cases, risk-free bonds now offer similar or better returns than rental properties, without the operational burden, vacancy risk, or illiquidity.

This shift is critical because investor demand was never permanent. It was conditional on the math working. Once that math breaks, capital moves elsewhere.

The data now shows exactly that. Investor purchases are falling sharply across multiple markets, with some metros seeing declines of 50 to 70 percent from peak levels. The same institutional buyers that helped drive prices higher are now stepping back, leaving a gap in demand that is beginning to impact market dynamics.

At the same time, inventory is rising. Without investor absorption, more homes are sitting on the market, increasing competition among sellers and creating early signs of downward price pressure.

Rent Growth Is Slowing. Returns Are Getting Squeezed

At the same time that financing conditions have worsened, the income side of the equation is also deteriorating.

According to CoreLogic data, rent growth across the U.S. has slowed to its weakest level in over 15 years (1.3% YoY from January 2025 to 2026). In many markets, rents are flat or declining on a year-over-year basis, particularly in areas that saw heavy investor and multifamily development during the pandemic boom.

This matters because investor returns depend on both price appreciation and rental income. Right now, both are under pressure.

Higher interest rates reduce affordability and buyer demand, while slowing rent growth limits income potential. That combination compresses yields and makes housing far less attractive as an investment compared to alternative assets.

In practical terms, the trade is getting squeezed from both sides. And when that happens, capital exits.

Investor Demand Is Collapsing in Key Markets

The impact is already visible in specific metros that were most dependent on investor activity.

In Atlanta, one of the largest investor-driven housing markets in the country, purchases are down roughly 70 percent from their peak, falling to the lowest levels in a decade in nominal terms. Similar patterns are emerging in Orlando and Las Vegas, where investor demand surged during the pandemic and is now sharply reversing.

These are not small markets. They were central to the housing boom.

Without investor demand, these markets now face rising inventory, weaker buyer competition, and increasing pressure on sellers to cut prices. This is where the shift is likely to show up first, but it will not be isolated. Other Sunbelt markets with similar dynamics could follow.

The implication is clear. The marginal buyer that helped drive prices higher is disappearing.

The Market Is Resetting. Track It in Real Time

What we are witnessing is not just a slowdown. It is a structural reset in how the housing market functions.

The era of Wall Street acting as a consistent buyer of U.S. housing may be ending. And as that happens, pricing dynamics are shifting back toward fundamentals, where supply, affordability, and local demand matter far more than institutional capital flows.

For buyers and smaller investors, this transition could create opportunities. As competition fades and inventory rises, negotiating power begins to shift back toward the individual.

But timing that shift is critical.

That is exactly why we built the Reventure App. You can track cap rates, rent growth and inventory trends across individual markets in real time, giving you a clear view of where returns are improving and where prices are most at risk.

If you want to understand where the housing market is headed next, start with the data.

Explore your market now on Reventure App.