Skyrocketing mortgage costs are a big problem for the U.S. housing market.

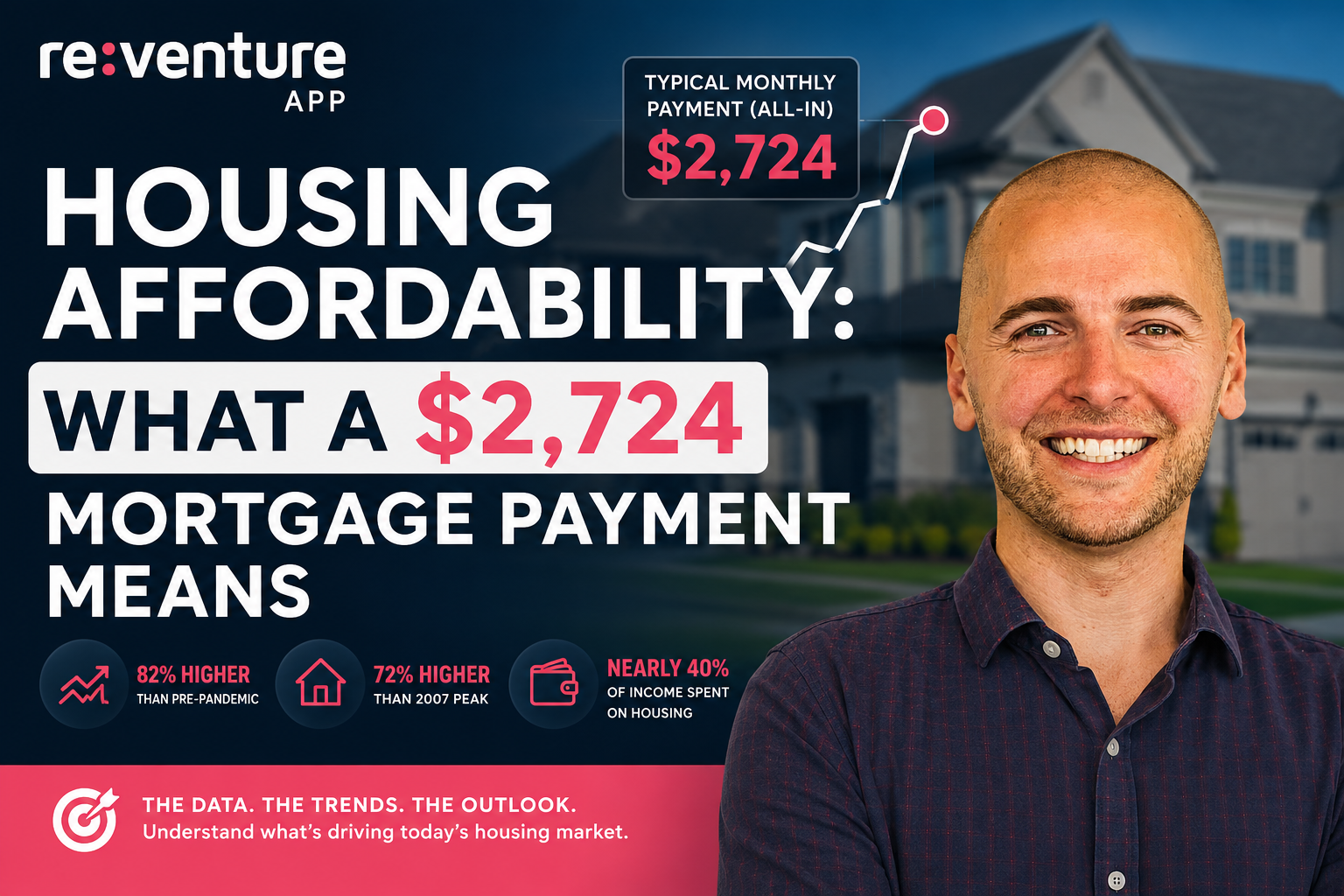

Housing affordability has reached its worst level in modern history, with the typical homebuyer now paying $2,724 per month to own a home, including the mortgage, property taxes, and homeowners’ insurance.

That’s an 82% increase since before the pandemic and 72% higher than the peak of the 2007 housing bubble.

For millions of Americans, homeownership is becoming increasingly out of reach.

The latest data from the Reventure App shows that mortgage payments have surged far faster than household incomes. As a result, the typical buyer now spends nearly 40% of their monthly income on housing payments, well above the long-term average.

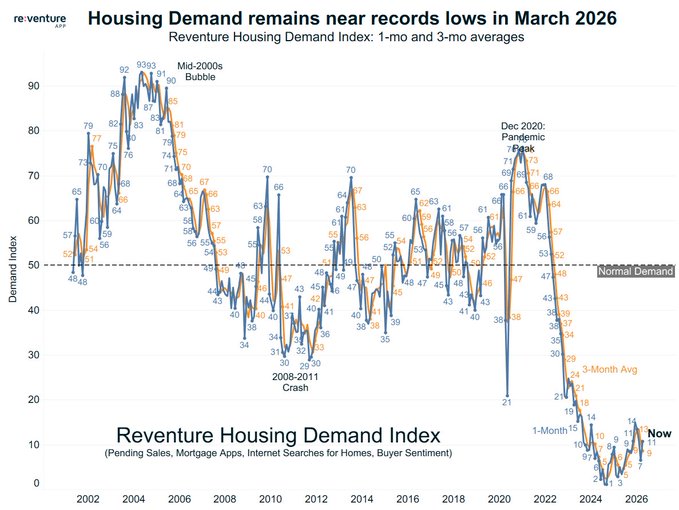

That imbalance is one of the biggest reasons home sales remain near multi-year lows despite a resilient job market.

Many people assume lower mortgage rates will solve the affordability crisis. But the data suggests otherwise.

While rates certainly matter, home prices have become the much larger driver of today’s record-high monthly payments.

Until affordability improves, buyer demand is likely to remain constrained across much of the U.S. housing market.

Housing Affordability Has Reached a Breaking Point

The numbers illustrate just how dramatically the market has changed. Before the pandemic, the typical monthly housing payment was about $1,489.

Today, buyers are paying more than $1,200 extra every month for a similar home.

Wage growth has helped offset part of that increase, but incomes simply haven’t kept pace with soaring home prices.

The result is a housing market where many qualified buyers can no longer afford to purchase. Others who can qualify are choosing to wait, hoping for better prices or lower mortgage rates.

That hesitation is reducing demand and slowing activity across many local housing markets.

Housing affordability has always moved in cycles, but today’s market stands out because both home prices and borrowing costs remain historically elevated.

Buyers are being squeezed from both directions, creating one of the least affordable housing environments in decades.

Home Prices Are the Biggest Driver of Housing Affordability

Many buyers blame today’s affordability problems entirely on mortgage rates. While higher borrowing costs have certainly increased monthly payments, they are only part of the story. The much larger factor has been the rapid increase in home prices since 2020.

Every increase in home values raises the amount buyers need to borrow. That larger loan balance increases monthly mortgage payments even if interest rates remain unchanged.

As prices climbed to record highs during the pandemic housing boom, affordability deteriorated at an equally rapid pace.

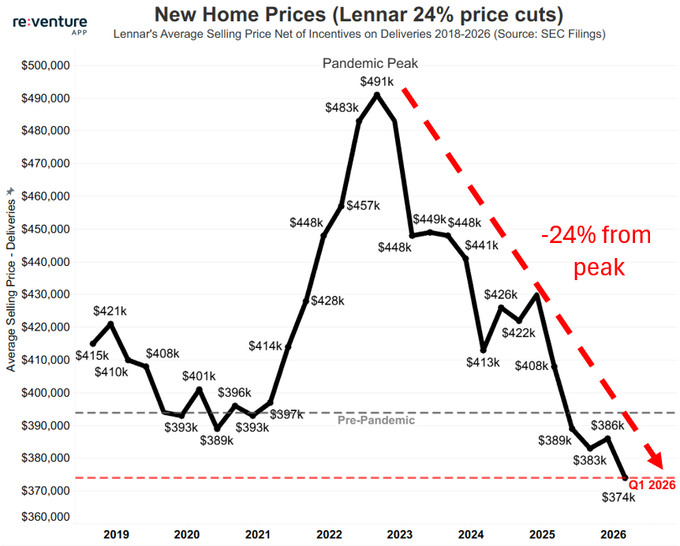

Lower home prices offer the fastest path toward restoring housing affordability.

Unlike income growth, which occurs gradually over many years, home prices can adjust much more quickly when supply begins to exceed demand. That makes prices the single biggest variable shaping today’s housing market.

Why Lower Mortgage Rates Alone Won’t Fix the Problem

The relationship between mortgage rates and affordability is often misunderstood.

Many buyers believe a return to 5.5% mortgage rates would immediately restore affordability.

While lower rates would reduce monthly payments, the improvement would be relatively modest compared to the impact of lower home prices.

The affordability matrix illustrates this clearly. If mortgage rates fell to 5.5% while home prices stayed unchanged, the typical monthly payment would decline to roughly $2,549.

By comparison, a 15% drop in home prices with today’s mortgage rates would reduce monthly payments much further, to approximately $2,325.

That comparison highlights why price adjustments matter so much. Mortgage rates influence affordability, but home prices determine the size of the loan buyers must finance.

Without meaningful price relief, affordability is unlikely to improve enough to bring large numbers of buyers back into the market.

Housing Affordability Won’t Recover Until Payments Fall Further

Improving housing affordability isn’t just about making mortgage payments slightly cheaper. The goal is to return monthly housing costs to a level that the average household can realistically afford over the long term.

One of the best ways to measure that is by looking at how much of a buyer’s income goes toward monthly housing payments.

The 30% Affordability Threshold Matters

The biggest challenge isn’t simply lowering monthly payments. It’s restoring them to a level that buyers have historically considered affordable.

Reventure’s affordability model shows that the typical household begins to re-enter the market when mortgage payments consume about 30% of household income.

Today, that figure remains well above that threshold.

Reaching a payment of roughly $2,150 per month would return the mortgage payment-to-income ratio to its long-term average.

Getting there, however, will require more than one favorable change. It would likely take a combination of lower home prices and lower mortgage rates, rather than relying on either factor alone.

The matrix shows why affordability remains such a difficult problem to solve. Even if mortgage rates decline modestly, payments stay elevated unless home prices also adjust.

That explains why many buyers continue delaying purchases despite expectations that borrowing costs will eventually fall.

The Mortgage Payment Burden Is Still Historically High

The mortgage payment-to-income ratio provides one of the clearest measures of housing affordability.

Today, the typical buyer spends 38.2% of household income on monthly housing payments. That’s an improvement from the post-pandemic peak above 41%, but it remains well above the long-term average of 30%.

Most of the recent improvement has come from rising household incomes rather than falling home prices.

Wage growth has helped ease affordability pressures, but not nearly enough to restore normal buying conditions. Until payments consume a smaller share of household income, demand is likely to remain below historical levels.

History also shows that affordability moves in cycles. Housing became expensive during the late 1980s, again during the 2006 housing bubble, and once more following the pandemic.

Each cycle was eventually corrected as prices, incomes, or interest rates moved back toward equilibrium.

Why Waiting for Income Growth Isn’t Enough

Some analysts believe higher wages will gradually restore housing affordability without requiring home prices to fall. While that is possible, it would likely take several more years.

Based on current income trends, it could be 2030 or later before affordability returns to historical norms through wage growth alone.

That’s a long wait for prospective buyers already struggling with today’s housing costs. It also means housing demand could remain subdued if affordability improves only gradually. Markets rarely return to balance when one side of the equation changes so slowly.

The faster solution would be lower home prices. Even modest price declines would reduce mortgage principal, lower monthly payments, and improve affordability much sooner than waiting for incomes to catch up.

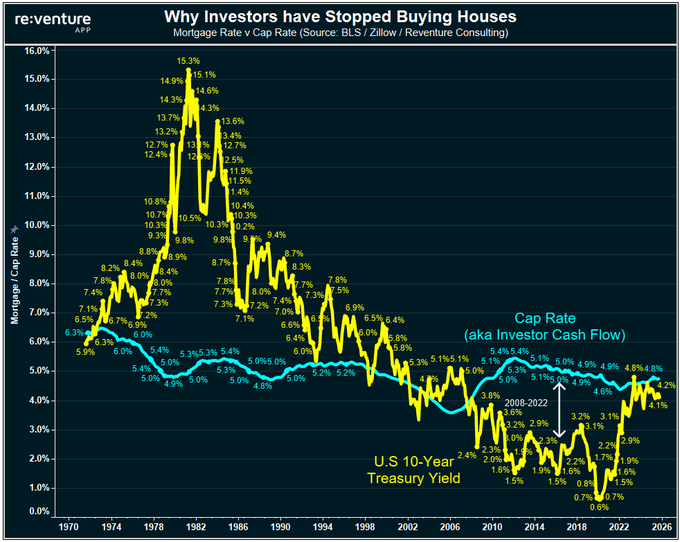

Mortgage Rates Are Likely to Stay Elevated

While lower home prices offer the quickest path to improving housing affordability, mortgage rates remain an important part of the equation.

Unfortunately for buyers hoping for relief, few signs that borrowing costs will decline significantly in the near future. That means affordability is unlikely to improve through lower rates alone.

Why Lower Mortgage Rates May Not Arrive Soon

Many buyers have spent the past four years expecting mortgage rates to fall sharply.

Despite changes in Federal Reserve policy, 30-year fixed mortgage rates have remained remarkably stable between 6% and 7%. That consistency suggests buyers shouldn’t rely on dramatically lower borrowing costs in the near future.

Meaningful declines in mortgage rates would probably require a significant economic slowdown or recession. While that remains possible, it is far from certain.

As a result, home prices may play a much larger role than interest rates in determining where housing affordability goes next.

Lower Home Prices Remain the Fastest Path to Better Housing Affordability

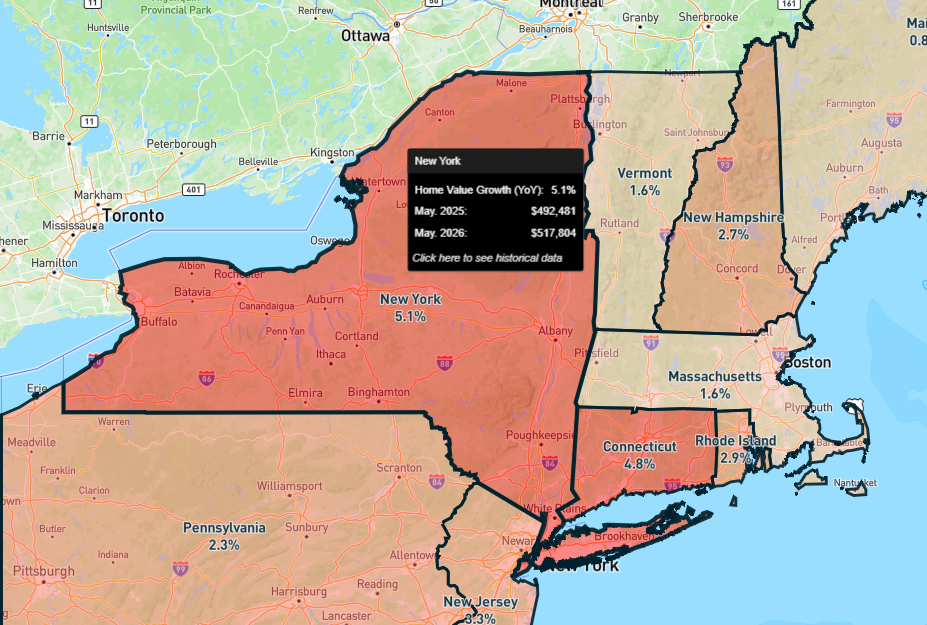

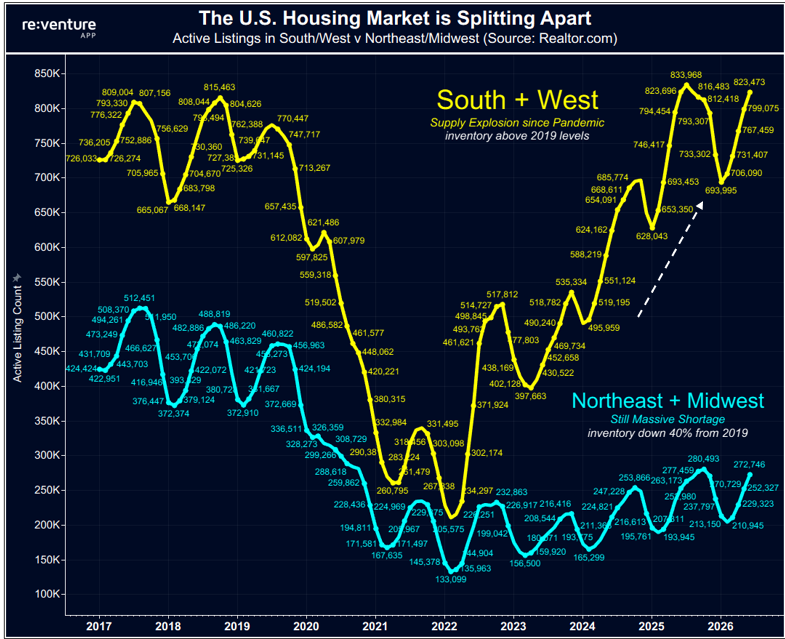

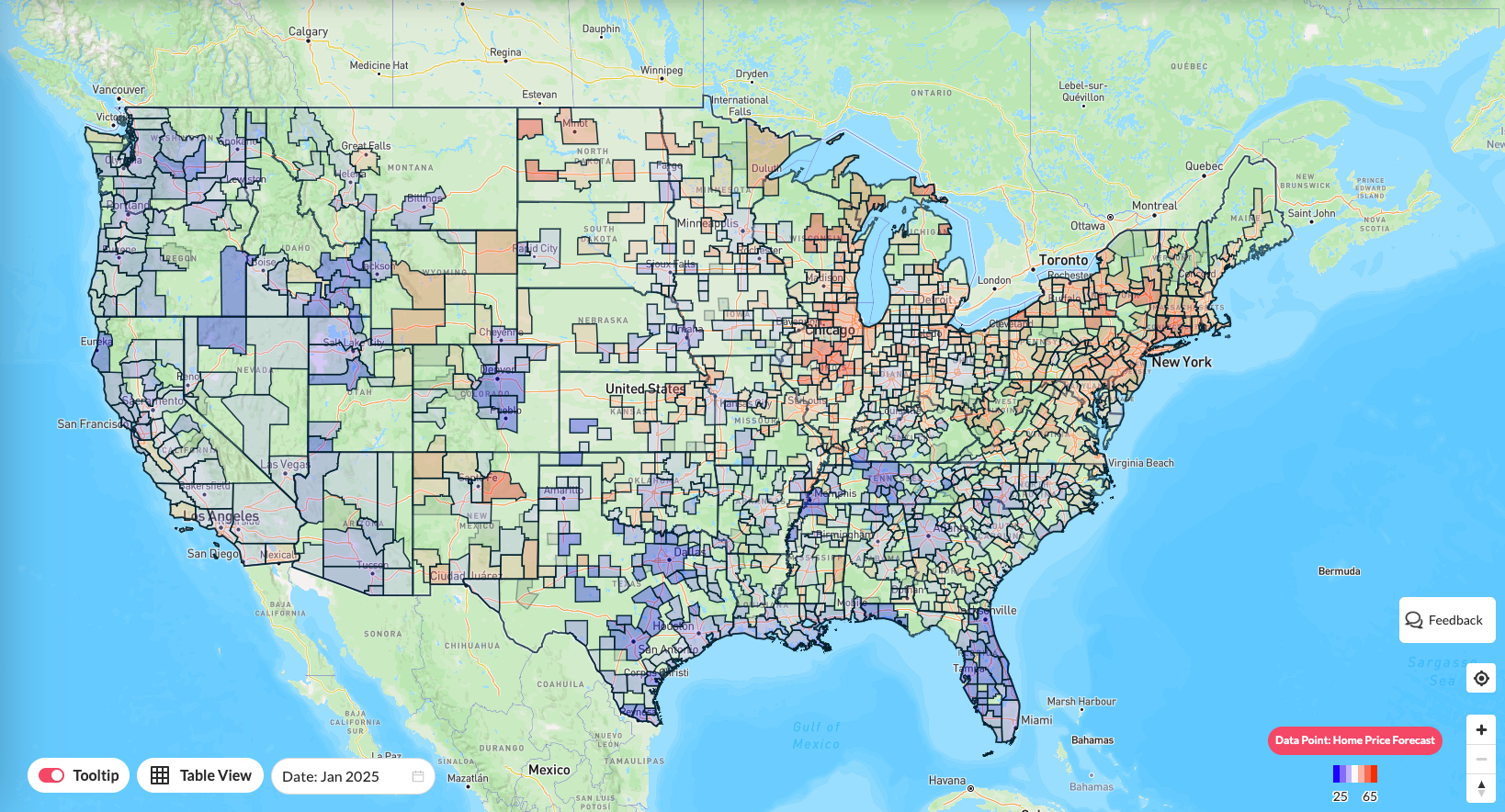

The latest Reventure App data show that home prices are already beginning to soften in parts of the South and West.

However, values remain firm throughout much of the Northeast and Midwest, creating one of the most divided housing markets in decades.

National averages no longer tell the full story.

Not every market will respond to declining affordability in the same way.

Some cities are already seeing meaningful price corrections, while others continue posting modest appreciation because of limited inventory and stronger local demand.

What Housing Affordability Means for Buyers

Housing affordability will likely determine the direction of the housing market over the next several years.

Until monthly payments move closer to historical norms, many buyers will remain on the sidelines, limiting demand and slowing market activity.

Whether affordability improves through lower prices, lower rates, stronger income growth, or a combination of all three, it will remain the most important housing metric to watch.

That’s exactly why we built the Reventure App.

You can track mortgage payments, housing affordability, home prices, inventory, and local market forecasts for your ZIP code, giving you a clearer picture of where affordability is improving and where prices remain stretched.

If you want to understand where the housing market is headed next, start with the data.

Explore your local market today with the Reventure App.

Frequently Asked Questions

1. How much house can I afford based on my income?

Most lenders recommend spending no more than 28% to 30% of your gross monthly income on housing costs. Your budget also depends on your down payment, mortgage rate, debts, property taxes, and homeowners’ insurance.

2. What is the mortgage affordability calculation?

Mortgage affordability is typically calculated by comparing your monthly housing payment to your gross monthly income. Most financial experts consider a home affordable when housing costs stay below 30% of household income.

3. How much is the monthly payment on a $275,000 mortgage?

The monthly payment depends on the mortgage rate, loan term, taxes, insurance, and down payment. At current market rates, a $275,000 mortgage generally results in a monthly payment of about $1,900 to $2,300, including taxes and insurance.

4. Why is housing affordability at its lowest level in decades?

Housing affordability has declined because home prices and mortgage rates increased much faster than household incomes. Higher borrowing costs combined with record home values have pushed monthly mortgage payments to historic highs.

5. Will housing affordability improve in 2026 and beyond?

Housing affordability is likely to improve gradually, but meaningful relief will probably require lower home prices, lower mortgage rates, stronger income growth, or a combination of all three.