Mortgage rates are stubbornly high. Home prices remain elevated. And incomes just aren’t keeping pace. That’s the story of today’s housing market. It’s not just about numbers. It’s about affordability slipping further away for everyday buyers.

Think about it. A few years ago, rates were near record lows. Monthly payments felt manageable. But now, with rates hovering above 6%, the same house costs hundreds more per month.

At the same time, median household income in the U.S. has barely budged. Prices and payments climb, while paychecks stand still. That mismatch is what creates the affordability crisis we’re all feeling.

So let’s put it into real numbers.

Say you want to buy a $400,000 home. You put 15% down. That leaves a $340,000 mortgage. With today’s 6.37% rate, plus taxes and insurance, your monthly payment lands around $2,703.

Stretch that out over a year, and you’re paying more than $32,000 just to keep the roof over your head. Here’s the kicker. Following the 30% rule of thumb, you’d need to earn over $108,000 per year to afford that house comfortably.

Read that again. $108,000. To buy what used to be a middle-class home.

This is why so many first-time buyers are on the sidelines. It’s not about wanting the dream less. It’s about the math making the dream harder to reach.

So if you’ve been feeling squeezed, you’re not imagining it. The numbers back you up.

Salary You Need to Earn to Buy a Home in America’s Largest Cities

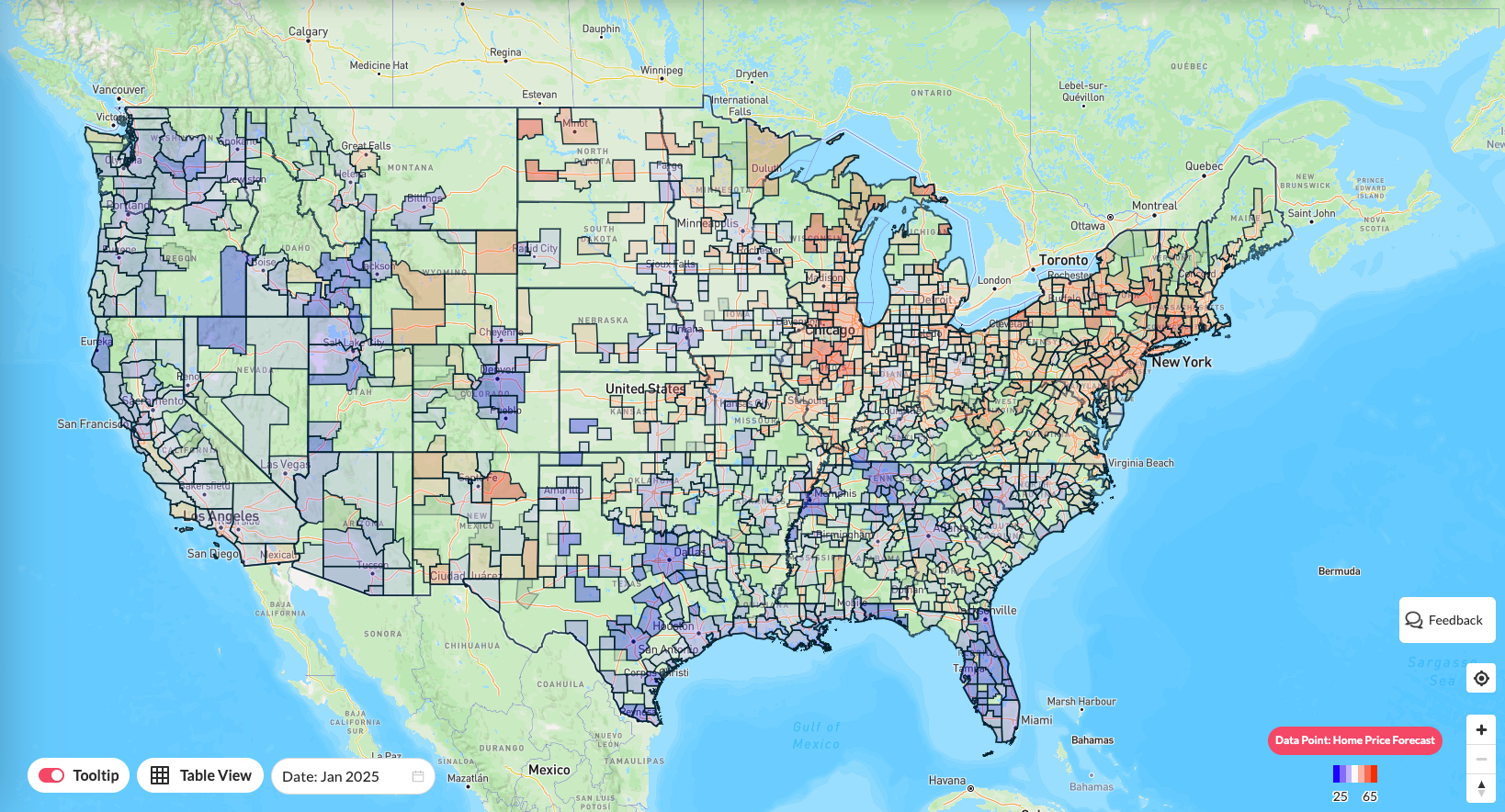

Reventure’s “Salary to Afford a House” metric shows just how expensive homeownership has become. It tells you exactly how much income you need to buy a home. And you can even see it down to the zip code.

The results are shocking. Let’s look at some of the largest U.S. metros:

1. New York, NY

In New York, you need $198,542 to afford a typical home. That’s nearly three times the U.S. median income. The monthly mortgage payment is close to $4,963. Taxes make it worse, with a 1.5% property tax rate. Home values are still rising, up 3.5% in the past year. Only 10.4% of listings have seen price cuts. Buyers here face little relief.

2. Detroit, MI

Detroit looks like a different world. You can buy with a salary of just $71,694. Payments average $1,792 a month. Taxes are higher at 1.2%, but the market is still affordable. Prices grew 3.4% year-over-year, yet almost 25% of homes had price cuts. Detroit remains one of the most accessible big cities for buyers.

It takes $238K in LA vs $72K in Detroit to afford a home. Access the above table here. [Link]

3. Miami, FL

Miami’s market has cooled. The salary to buy is $122,332. Mortgage payments run about $3,058. Prices actually fell 4.2% year-over-year. Still, 20.2% of sellers are cutting prices. For locals, affordability is tough, but at least the trend is bending in the right direction.

4. Chicago, IL

Chicago sits in the middle. Buyers need $99,908 to purchase. The average mortgage payment is $2,497. Property taxes are steep at 1.9%. Home values are up 3.3%, but 21.6% of listings are dropping prices. Chicago is more attainable than coastal cities, but it is still costly for many families.

The Big Picture

The gap is massive. In Detroit, you need $71,000. In New York, it is almost $200,000. Same dream. Different reality. Reventure’s data makes one thing clear. Some metros still offer opportunity. Others have priced out the middle class.

That’s why having local, zip-level data matters. One side of a city might look affordable, while the other is completely out of range. And that’s exactly what you get with Reventure’s premium plan. So, get yourself Reventure’s premium plan for just $49/ month.

And unlock zip-code insights, inventory trends, and price projections. The forecasts are performing six times better than Zillow’s. Plus, get 40+ premium data points. Think about it. That’s less than 0.02% of the cost of buying a home. Yet it could be the difference between landing the right property or missing out. Between making a deal and watching it fall through.

If the numbers we’ve just walked through surprised you, wait until you see what’s happening in your own neighborhood.

One Response