Why You Shouldn’t Expect Mortgage Rates to Drop Anytime Soon (7% is the new normal)?

May 22, 2025

May 22, 2025

If you’re waiting for mortgage rates to fall, you might want to stop holding your breath. The U.S. housing market has entered a phase where 7% mortgage rates may not just be a temporary spike; they could represent the new baseline.

According to a recent analysis by Reventure Consulting using Federal Reserve data, the spread between mortgage rates and inflation, a key metric that measures how much more borrowers pay above inflation, is now 4.4% in 2025. This is nearly in line with the long-term average of 3.7% dating back to 1955.

The mortgage rate–inflation spread in 2025 has returned to its 70-year average, reinforcing that today’s 7% rates are historically normal. Access the above graph here. [Link]

Nick Gerli, CEO of Reventure App, explains: “Want mortgage rates to drop? It’s unlikely to happen. Because the Mortgage Rate / Inflation spread for the U.S. economy is now back to its long-term 70-year average.”

With inflation currently around 2.5%, today’s 7% mortgage rates are not unusually high. In fact, they are historically consistent with the average spread seen across decades of economic data.

“This indicates that the current mortgage rate environment is actually fairly normal for the current level of inflation,” Gerli adds. “So perhaps we get a little relief in the future. But not a whole lot. There’s also the chance inflation picks back up, which would also put a floor on rates.”

In short, 7% isn’t elevated. It’s a historical reality.

America’s Mortgage Burden is Becoming Unmanageable in High-Cost States in 2025

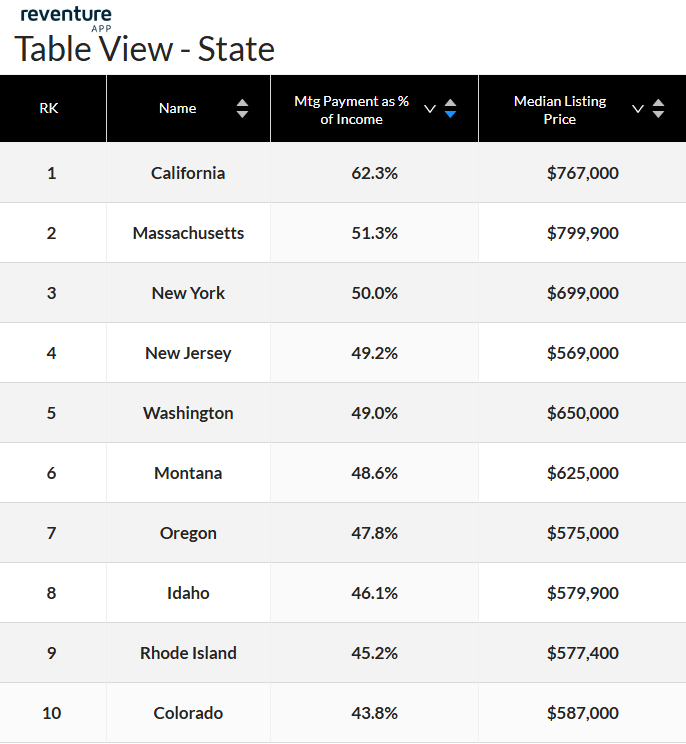

As mortgage rates stabilize around 7%, the financial strain on buyers is becoming more visible, especially in states with expensive housing markets. New data available on Reventure App shows that in some regions, homeowners are spending well over half of their income just to cover mortgage payments.

California tops the list, where the median home price is $767,000 and the typical mortgage payment now eats up 62.3% of household income. This level of cost burden is unsustainable for many, especially first-time buyers.

Homebuyers in states like California and Massachusetts are now spending over 50% of their income on mortgage payments amid elevated home prices. Access the above table here. [Link]

Massachusetts follows closely with a 51.3% mortgage-to-income ratio and a median listing price of $799,900, the highest on the list. New York isn’t far behind, where buyers spend 50% of their income to afford homes priced at $699,000.

New Jersey, Washington, and Montana all hover just below that threshold, with mortgage burdens between 48.6% and 49.2%, despite varying home prices. Even less populated states like Idaho (46.1%) and Montana (48.6%) are seeing elevated cost ratios.

Rounding out the top ten are Oregon (47.8%), Rhode Island (45.2%), and Colorado (43.8%), where home prices remain above $575,000 across the board.

In these states, affordability is no longer just about interest rates, it’s about wages failing to keep pace with home prices and borrowing costs combined.

Homes Are Sitting Longer on the Market in 2025

As borrowing costs remain high, buyer activity has slowed, and homes are staying on the market longer. The Days on Market (DOM) metric is rising across several states, indicating a cooling in demand.

Florida now leads the country with homes taking an average of 69 days to sell, up 12.2% year-over-year. Louisiana (68 days, +9.6%) and Mississippi (66 days, +15.7%) follow closely, confirming a regional softening in the South.

Homes are sitting longer on the market in 2025, with Vermont, Mississippi, and Florida seeing double-digit increases in time to sell. Access the above table here. [Link]

Vermont saw the sharpest DOM growth, up 17.2% from last year, with homes sitting for 65 days. Even states like New Mexico (+8.4%) and Maine (+4.4%) are showing upward trends.

Montana holds steady at 57 days, but states like Wyoming are outliers, showing a decline in DOM by 11.7%, suggesting continued activity in low-inventory markets. Rising DOM typically reflects reduced buyer urgency, and when paired with affordability challenges, it hints that price cuts may follow in slower-moving markets.

Moreover, if you require ZIP code-level information of a specific state’s housing situation, sign up for Reventure Apps’ premium plan for just $39/ month. Get exclusive access to various market metrics across any state, metro, county, or ZIP code in the U.S.

FAQs about Mortgage Rates in 2025

1. Why Are Mortgage Rates Still High in 2025?

Mortgage rates remain around 7% because the spread between mortgage rates and inflation has returned to its 70-year average of 3.7%. With inflation at 2.5%, today’s rates are historically normal, not unusually high.

2. How is Affordability Impacting the Housing Market?

In high-cost states like California and Massachusetts, mortgage payments now exceed 50% of household income. This has led to reduced buyer demand, causing homes to sit longer on the market and indicating a potential price correction in overheated areas.