Something strange is happening in the US housing market. People aren’t selling, even when they want to. And one big reason is sitting quietly on their balance sheets, meaning home equity loans.

Over the last two years, Americans have built record amounts of equity. But tapping that wealth has become costly. Borrowers are locked into 7–9 percent rates, and many hesitate to refinance their cheap first mortgages. The result?

A frozen market. Fewer listings. Fewer moves. And a growing divide between homeowners with trapped equity and buyers stuck waiting outside. Let’s find out more about it:

1. Homeowners Are Stuck and So Is the Market

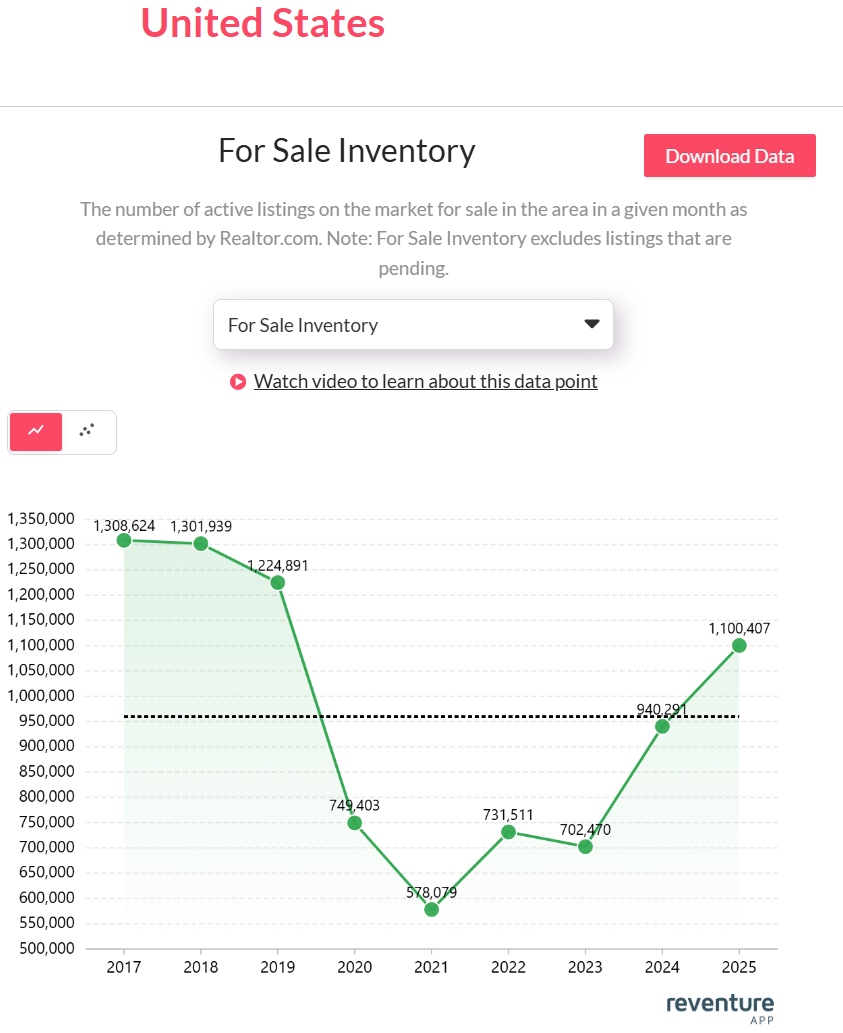

Something strange is happening in housing. Inventory has risen, but the market still feels frozen. Active listings have surged to 1.1 million in 2025. And that is almost double the pandemic low of 578,000, according to Realtor.com data available on Reventure App. Yet homes aren’t exactly flooding the market. That’s because new supply isn’t coming from willing sellers. It’s coming from forced ones.

Active listings jumped to 1.1 million in 2025, nearly double the pandemic low. Yet the market still feels frozen. Access the above graph here. [Link]

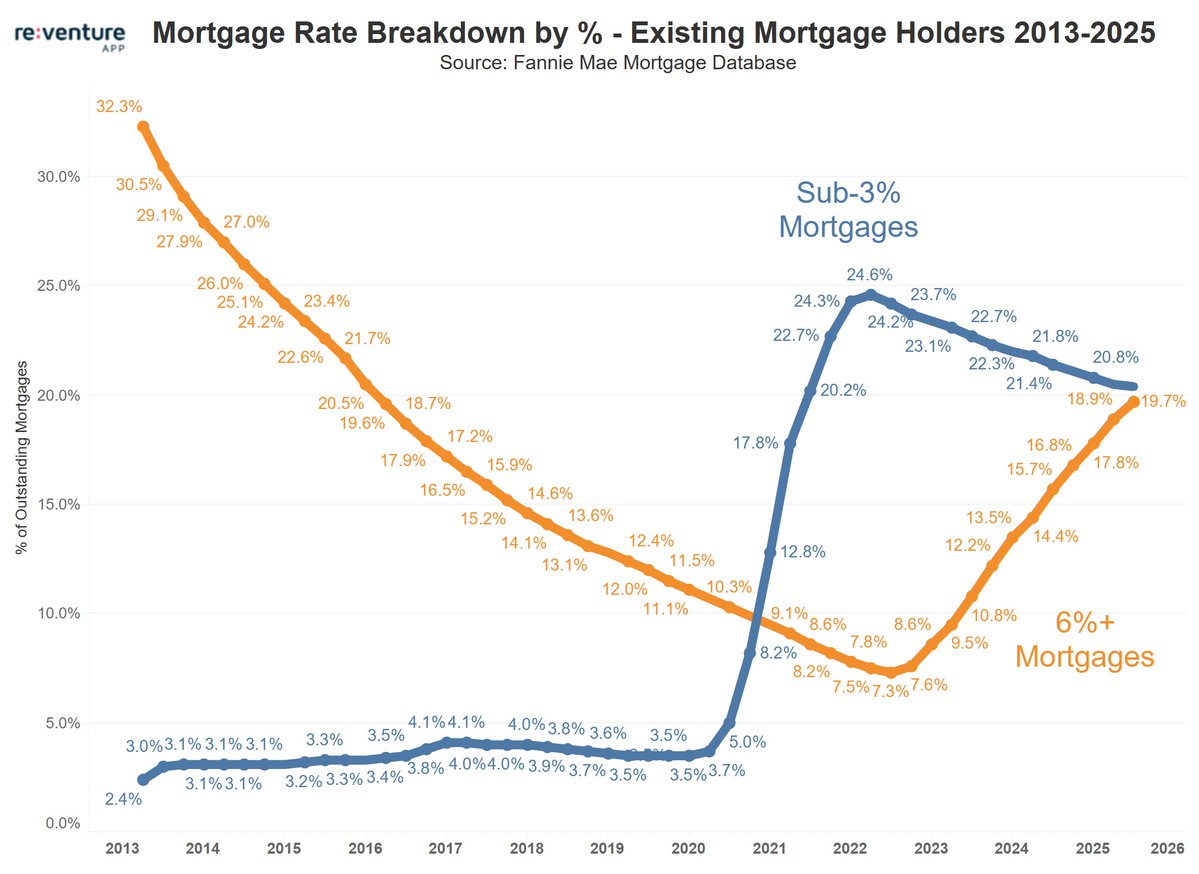

Millions of homeowners remain locked into 2–3 percent mortgage rates from the pandemic era. Selling now would mean swapping a cheap mortgage for one nearly triple the cost. Even with rising equity, tapping that wealth through home equity loans or HELOCs is equally painful. Borrowing costs are around 8 percent, discouraging anyone from cashing out.

This standoff between low-rate homeowners and high-rate buyers is keeping inventory historically tight. The result? A market that’s technically thawing on paper but frozen in motion. Every uptick in listings only reveals how few people are actually moving.

2. Incomes Are Rising, but Not Fast Enough to Buy Freedom

Median household income in the U.S. reached $83,200 in 2025, marking a steady climb from $77,700 in 2023 and nearly doubling since 2005. On paper, that sounds promising. In reality, it’s not enough to offset the crushing weight of housing costs.

Mortgage payments on a typical home now consume close to 40 percent of the median household’s income, up from about 25 percent just five years ago.

U.S. median household income climbed to $83,200 in 2025. But rising pay hasn’t caught up with record housing costs. Access the above graph here. [Link]

The Federal Reserve’s long period of elevated interest rates has kept affordability at record lows despite the recent softening in prices. Homebuyers who waited for relief are still finding that higher paychecks can’t bridge the gap created by expensive debt.

At the same time, homeowners who might have once traded up can’t justify new monthly payments that would erase their equity gains. Many are choosing to stay put, renovate, or borrow modestly instead of moving.

3. Renters Feel the Squeeze Too

In 2025, rent consumes 29.1 percent of the average household’s income, down slightly from the 2022 peak of 30.3 percent but still far above pre-pandemic norms. The pressure is visible everywhere. From suburban apartments to urban single-family rentals as landlords pass along higher maintenance and insurance costs.

Rent now consumes 29.1 percent of income. Easing slightly from 2022’s peak, yet still squeezing renters nationwide. Access the above graph here. [Link]

What’s more, low home sales have spilled over into the rental market. With fewer homeowners moving, would-be buyers are staying renters longer, tightening rental supply and propping up prices. This creates a feedback loop: homeowners won’t sell because rents and replacement homes are too costly, while renters can’t buy because prices and rates remain too high.

The result is a frozen flow of housing mobility. Renters aren’t graduating into ownership, and homeowners aren’t vacating starter homes for larger ones. Even though equity levels across the country total more than $17 trillion. Very little of it is circulating.

Until borrowing costs ease meaningfully and incomes outpace both rent and mortgage inflation, the housing market will remain a picture of pent-up motion. Where wealth exists, but few can afford to move it.

Final Thoughts

The real story lies in home equity. Who holds it, who can’t tap it, and who’s priced out because of it. Every metro tells a different version of the same freeze. Some are seeing listings tick up, while others remain locked in by 3 percent mortgages and 8 percent equity loan rates. And even renters aren’t escaping the squeeze, with rent still taking nearly 30 percent of income nationwide.

To see exactly how equity, affordability, and inventory are shifting in your area, explore the data on Reventure Premium. It’s just $49 a month and gives you 6x better forecast than Zillow.

And you will be able to unlock 40+ data points, from income-to-value ratios to inventory growth and rent burdens. In a market this tight, timing and local insight matter more than ever. Knowing where homeowners are trapped and where opportunity is finally unlocking could make all the difference in your next move.