The Trump Administration is floating an idea, and they’re hoping it could help improve housing market affordability: the 50-year mortgage.

Proponents of the idea point to its ability to lower mortgage payments and increase short-term affordability, and champion as a much better alternative then renting. While critics suggest the 50-year mortgage is tantamount to a “debt trap” and will drive up borrowing costs in the long-run.

So what’s the truth? Reventure broke down the numbers and found the 50-Year Mortgage would actually save homebuyers money compared to renting, but only after 17 years. Meanwhile, there are a variety of risks associated with the 50-Year Mortgage, outlined below.

What is a 50-Year Mortgage, exactly?

Technically speaking, a mortgage can be over any duration of term.

A 50-Year Mortgage is one that takes 50 years to pay off based on its amortization schedule. The standard mortgage is 30 years. And there are even shorter options available for borrowers at higher monthly payments.

The shorter the term, the higher the payment is because the mortgage needs to be paid off faster. The longer the term, the lower the payment is, as there’s more time to pay off the mortgage.

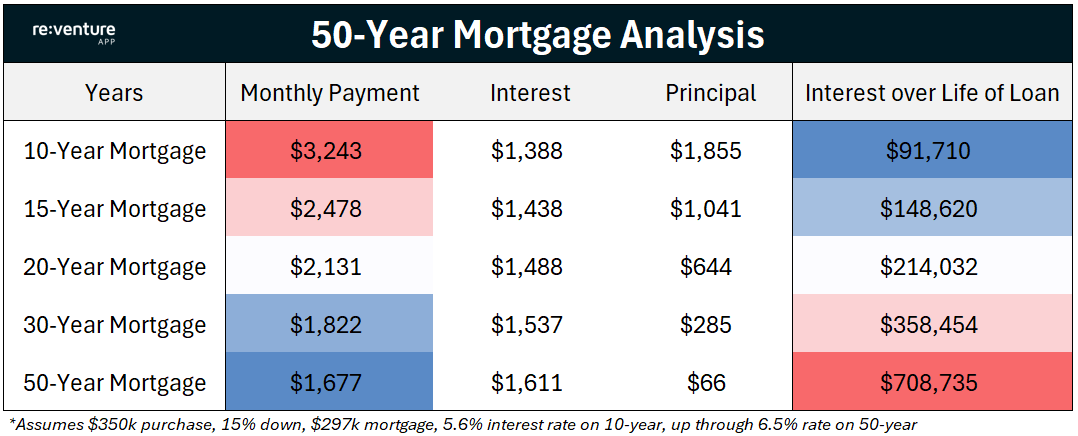

You can see that a theoretical 50-Year Mortgage, on a $350,000 home purchase with 15% down ($297,000 principal), would yield a monthly payment of $1,677/month. Which is about half of what the monthly payment would be on a 10-Year Mortgage for the same house. You can also see the 50-Year Mortgage has an 8% lower monthly payment than the 30-Year Mortgage.

However, there’s a catch. And it’s a big one. If someone takes out a 50-year mortgage, and holds it to maturity, then their total interest paid over the life of the loan will be $708,000, more than double the total interest paid of the 30-year mortgage.

And more than triple the interest paid on a 20-year mortgage. And more than 500% higher than the interest paid on a 10-year mortgage, which is only $92,000.

This is why critics of the 50-year mortgage, like Marjorie Taylor Greene, think it amounts a reward for banks and can cause people to be “in debt forever, in debt for life”.

The 50-Year Mortgage Controversy

Herein lies the controversy with the 50-year mortgage: its lower monthly payment will allow more buyers to qualify, getting more households into homeownership. On the surface, that sounds like a good thing — and it’s likely the main reason why Trump and Pulte are pushing for it.

However, this “affordability” is an illusion. The payment is only lower because almost none of it goes toward principal. In fact, at the start of a 50-year mortgage, only about 4% of your payment goes toward paying down the loan balance. By comparison, on a 30-year mortgage, over 15% of the payment builds equity from day one. That principal portion acts as a kind of forced savings account — ensuring borrowers gradually build wealth and don’t overextend themselves.

To see why this matters, consider a simple example. On a $297,000 loan, after 10 years:

-

A 50-year mortgage borrower would still owe roughly $286,000, having paid down only about 4% of the loan.

-

A 30-year mortgage borrower, on the other hand, would have reduced their balance to around $250,000, building a meaningful equity cushion.

That difference can be the difference between stability and being stuck. If home prices fall — as we’re already seeing in Florida and Texas in 2025 — 50-year borrowers could find themselves trapped in negative equity, unable to sell without bringing cash to the table.

In other words, while the 50-year mortgage might expand short-term affordability, it risks trading long-term financial security for short-term qualification — a dangerous swap in a market that’s already showing signs of decline.

Access our Home Price Forecast for your ZIP Code on Reventure App

The Long Game: 50 Year Mortgage v Renting

But let’s play devil’s advocate for a second. Could there be a situation where for a 50-Year Mortgage is a good idea, even if it does result in higher long-term interest cost and reduce the equity-building component to owning a home? And could Trump and Bill Pulte be onto something with this suggestion?

To fairly evaluate the 50-year mortgage, we need to compare it not just to a 30-year loan — but to the cost of renting for 50 years, which is the likely alternative for many renters priced out of today’s market.

The key advantage of a 50-year fixed mortgage is payment stability. Once locked in, the borrower’s principal and interest payment won’t rise with inflation. Over time, that fixed payment becomes cheaper in “real” terms, while rents typically climb higher year after year. Of course, this stability comes with a trade-off: higher interest rates and slower equity accumulation than shorter loans.

Let’s quantify that. And start with some assumptions: $350,000 home purchase, with a 15% down payment and a corresponding $297,000 mortgage at a 6.5% interest rate. Property taxes and insurance calculated at 2.0% of home’s value to start, grown at 0.2% per month compounded.

If the borrower holds the loan to full term, they’ll pay roughly $1.39 million in total interest, tax, and insurance costs to live in and own the home over 50 years.

Now compare that to renting the same home today for $1,850/month, with rent rising at the same 0.2% monthly pace. Over 50 years, that renter will spend $2.15 million in total rent — 55% more than the total cost of owning with a 50-year mortgage.

That’s the paradox:

-

In the short term, the renter wins. For roughly the first 17 years, renting remains cheaper month-to-month.

-

In the long term, the homeowner wins. Once inflation compounds, the fixed mortgage payment becomes a bargain compared to rent — even with the enormous interest cost.

Will the 50-Year Mortgage increase Systemic Risk in the Housing Market?

However, the 50-year mortgage could also introduce new systemic risks. The borrowers most likely to take this loan will be income- and cash-constrained, making them more vulnerable to default.

And that raises a troubling question: what happens when these borrowers can’t pay?

It’s not hard to imagine policymakers stepping in with foreclosure moratoria, just as they did during the pandemic. While well-intentioned, those policies reduced market inventory and made affordability worse overall.

If the government introduces a 50-year mortgage program, there must be explicit guardrails to prevent this. Borrowers must understand that a mortgage is a financial contract, not a permanent housing guarantee. Without strict limits, the program risks turning into a system of “renting from the government” rather than true homeownership.

The Downpayment Requirement

Finally, since 50-year borrowers won’t be building equity quickly through principal payments, they should be required to bring more equity upfront.

A minimum down payment of 10%, and ideally 15%, would give borrowers a meaningful cushion against price declines — ensuring that even if home values dip, they’re not immediately underwater.

This also means that a large share of borrowers under the FHA’s first-time homebuyer program would not qualify, since these buyers typically only bring 3–5% down. But that’s precisely the point. Establishing a minimum down payment of at least 10% would help ensure stronger credit quality, reduce default risk, and limit future taxpayer exposure to potential bailouts stemming from higher foreclosures.

If the goal of the 50-year mortgage is to expand access responsibly, this type of up-front discipline is essential — otherwise, we risk repeating the same mistakes of prior housing cycles where easy credit led to speculative excess and financial instability.

The Final Word

We still don’t know how serious the Trump administration is about enacting a 50-year mortgage. If they push forward with it, it will likely require approval from Congress, since the Housing Economy and Recovery Act (2008) and National Housing Act (1934) stipulate the type of mortgages that the Fannie Mae, Freddie Mac, and the FHA can issue. In the meantime, private lenders are free to offer 50-year mortgages, and some might be doing so already.

Any housing market impact from the potential enactment of a 50-Year Mortgage option would be tracked in Reventure’s forecast, as positive impacts on buyer demand would show up in inventory, price cuts, and days on market. If you haven’t done so already, make sure to upgrade for the Reventure Premium plan, so you can see the 12-month forecast in your ZIP code and get ahead the market.

Our home buyers and investors are savings thousands, even tens of thousands, using our forecasts to help negotiate better purchase prices and making better buying decisions. Upgrade now at http://www.reventure.app.