If you’ve been following the U.S. housing market, you can feel the shift. The golden era of ultra-cheap mortgages is ending. For years, homeowners locked in rates below 3%, fueling one of the hottest housing booms in history. But that balance is now reversing.

Nick Gerli, CEO of Reventure App, shared new data from Fannie Mae showing just how dramatic the change is. Sub-3% mortgages, once dominant, are steadily falling. Meanwhile, 6%+ mortgages are surging upward.

The data shows that the market is in transition. A few years ago, nearly one in four homeowners enjoyed rates under 3%. Now, that share is shrinking fast. By late 2025, more Americans will hold 6% loans than the historic sub-3% ones.

We’re entering a new phase. A phase defined by affordability struggles, slower movement, and fewer incentives to sell. The mortgage market is flipping, and it’s changing how Americans think about buying and staying in their homes. Let’s figure out more about it:

From Sub-3% to 6%+ – What the Numbers Show

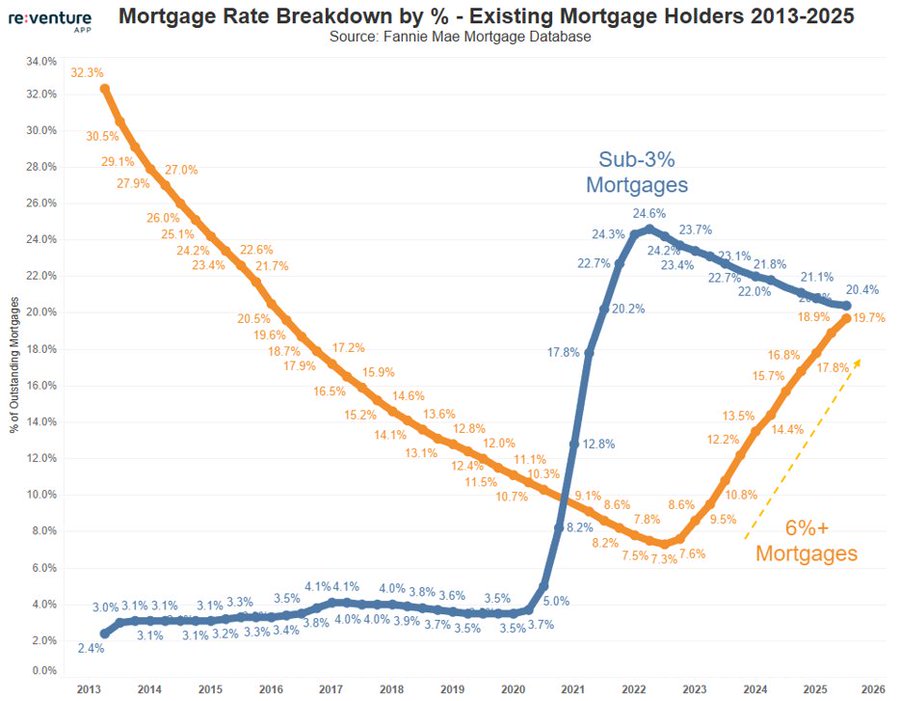

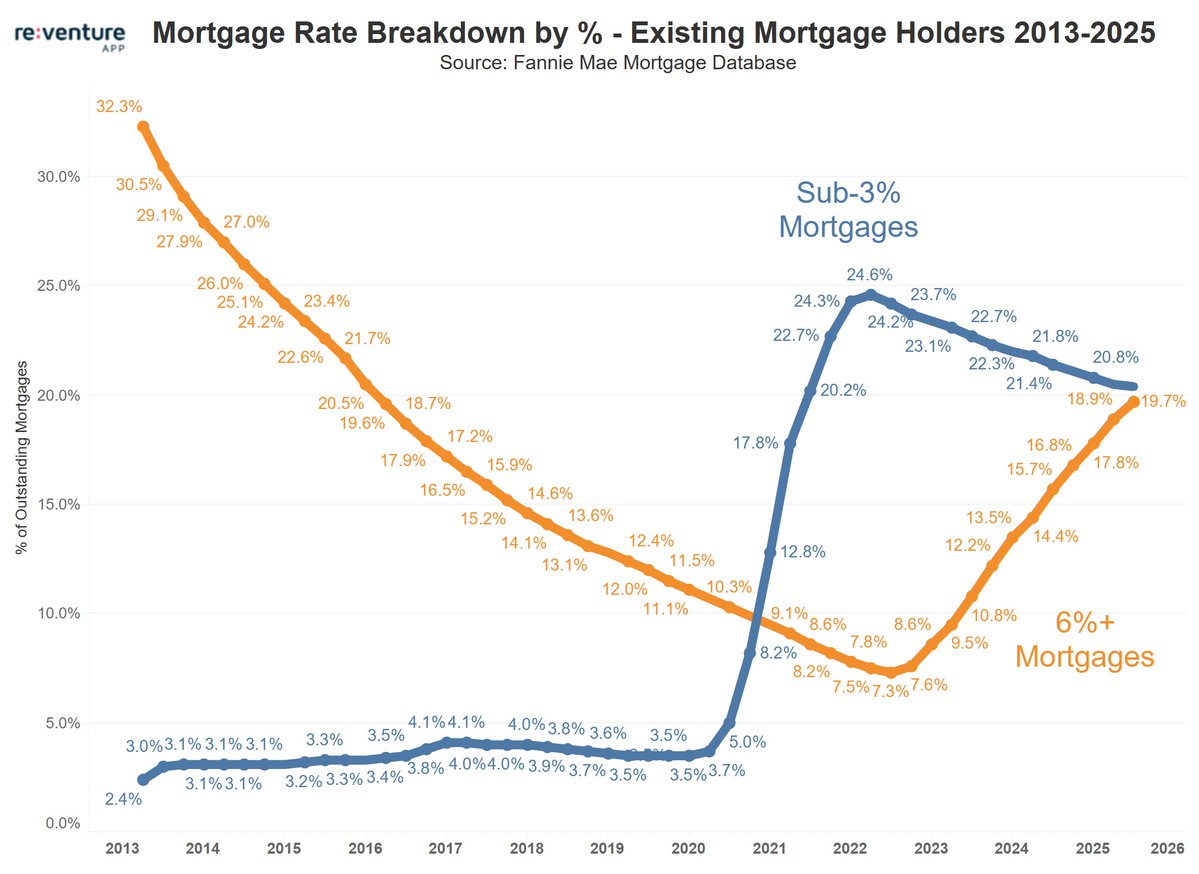

Look closely at the chart below, and see the clear story. In 2021, sub-3% mortgages peaked at about 24.6% of all outstanding loans, i.e., nearly a quarter of the market. That was the height of the low-rate era when buyers rushed to lock in deals under 3%.

But since then, that blue line has been falling fast. By 2025, sub-3% mortgages are projected to shrink to around 20.4%. While the share of 6%+ mortgages, shown in orange, climbs sharply. From barely 7.3% in 2022, these high-rate loans have surged to nearly 18%, with projections pushing beyond 19% by 2025.

Mortgages with rates above 6% are expected to overtake those with rates below 3% by late 2025, marking the end of the ultra-low-rate era. Access the above graph here. [Link]

That’s a crossover point. The moment when expensive loans outnumber cheap ones. It reflects how quickly mortgage conditions have normalized after pandemic lows.

The contrast is striking. In 2013, 6%+ mortgages dominated at 32% and by 2021, they almost vanished. Now they’re roaring back. This U-turn in rates reshapes everything. From home affordability to mobility, it shows just how sensitive the housing market is to interest-rate cycles.

Why This Shift Matters for Homeowners and Buyers?

1. The ‘Rate Lock’ Effect

Millions of Americans are now stuck with sub-3% mortgages. For them, selling and buying again at today’s 6–7% rates would mean doubling their monthly payments. This “rate lock” discourages movement.

Homeowners prefer to stay put, which keeps inventory tight and limits supply for new buyers. That’s a major reason listings remain historically low, even as demand cools.

2. Refinancing Becomes Rare

During the pandemic, refinancing was a national sport. Low rates meant easy savings. But now, with rates doubling, refinancing has nearly vanished. Homeowners who are already locked in cheap loans have no reason to refinance.

Unless they need cash for renovations or debt consolidation, that’s a big slowdown for lenders and the broader credit market.

3. Affordability Crunch for New Buyers

For first-time buyers, the shift is painful. Higher mortgage rates mean higher monthly payments and stricter qualification standards. The average homebuyer can now afford 30–40% less house than in 2021.

4. The Bigger Picture

As the current data shows, the rise of 6%+ mortgages highlights the end of easy money. It’s reshaping buyer psychology, slowing sales, and redefining what ‘affordable’ really means in today’s housing market.

Final Takeaway

The mortgage market is changing fast. Staying informed isn’t just helpful anymore; it’s crucial. If you’re a homeowner, knowing when to refinance can save you thousands.

If you’re a buyer, timing your move can make or break your budget. Trends like the 6% crossover can flip local markets overnight. Keep an eye on the data, because the right insight at the right time can be the edge you need.

So, get yourself a monthly premium subscription for only $49. It gives you six times more accurate forecasts than Zillow. And you will be able to unlock 40+ data points, from income-to-value ratios to inventory shifts and price projections. For anyone serious about buying in the right place at the right time, that data could make all the difference.

One Response