Owning a home has long been a sign of stability in America. Families often viewed buying as a milestone, a step toward building wealth. But in 2025, the numbers tell a different story. The cost of carrying a mortgage has climbed far above the cost of rent.

On average, a typical monthly mortgage now runs close to $2,750. Renting, by comparison, costs about $2,000. That $750 gap each month adds up quickly. It leaves many asking a hard question: should you stretch to buy, or save money and rent instead? The answer isn’t as simple as it once was.

Let’s get into the details:

The Cost Landscape in 2025

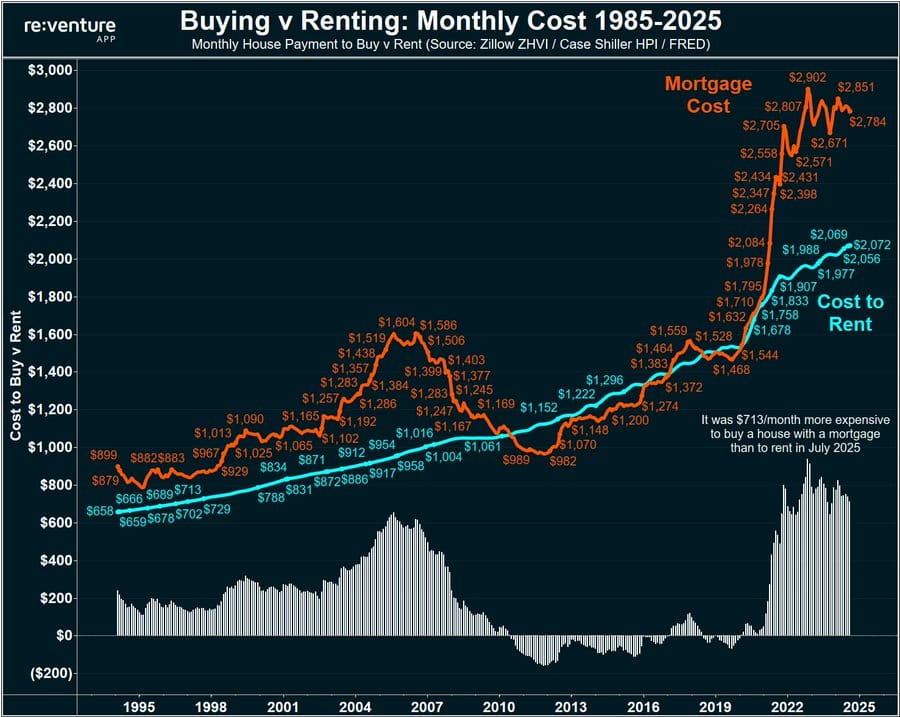

The gap between owning and renting is striking in 2025. According to Reventure’s calculations, the average monthly cost to buy a home with a mortgage in July was $2,784. By comparison, Zillow’s rental index puts the average monthly rent at $2,072.

That’s a difference of $713 every month. Over the course of a year, the premium adds up to more than $8,500. It is also one of the largest gaps ever recorded. On a percentage basis, buying now costs about 34% more than renting.

In July 2025, buying a home with a mortgage cost $713 more per month than renting, one of the widest gaps ever recorded.

For many households, that math is impossible to ignore. First-time buyers, in particular, are feeling the squeeze. Higher interest rates, insurance, and taxes push monthly mortgage costs far beyond what renters pay. The result is a slowdown in buyer demand across much of the country.

Moreover, many younger families and working professionals are putting their home-buying plans on hold. They save hundreds of dollars a month, money that can go toward savings, investments, or simply making ends meet.

Pros and Cons of Buying in 2025

Now, the cost gap is clear, but price alone doesn’t settle the debate. Buying still offers long-term benefits, while renting offers short-term relief. To understand the choice, it helps to look at both sides.

Pros

- Owning a home means building equity. Each payment chips away at the loan and adds to your stake in the property. That money isn’t disappearing like rent.

- A fixed-rate mortgage also brings stability. While rents can rise every year, your monthly payment stays the same. For many, that security matters.

- There are also tax benefits that can ease the load.

- And let’s not forget the pride of ownership. Having a place that is truly yours carries value that numbers don’t fully capture.

- If the housing market rebounds, buyers also stand to gain from appreciation.

Cons

- The drawbacks, though, are hard to ignore. Upfront costs are steep, from the down payment to closing fees.

- Maintenance never stops and adds to the bill.

- Flexibility is limited too. Selling or moving is not easy if plans change.

- And in 2025, the biggest con is simple. The mortgage payment is hundreds higher than rent.

- Add to that the risk of falling home prices in some regions, and buying feels like a gamble for many households.

Pros and Cons of Renting in 2025

After weighing the costs and risks of buying, it’s only fair to look at renting. For many households in 2025, renting is not just a temporary step. It can be the smarter choice, depending on your financial situation and lifestyle.

Pros

- The first advantage is simple: rent is cheaper. At an average of $2,072 a month, it saves hundreds compared with a mortgage. That extra cash makes a difference. Families can use it for bills, savings, or even a vacation.

- Renting also gives freedom. If a new job opens in another city, it’s easier to move. No long selling process. No waiting for buyers.

- Another plus is peace of mind on repairs. When something breaks, the landlord pays, not the tenant. This keeps monthly costs predictable.

- Finally, renters can invest the money they save. Stocks, savings accounts, or even starting a business are options.

Cons

- The downside is clear. Rent money doesn’t build ownership. Once it’s paid, it’s gone. Landlords can raise prices at the end of a lease.

- Rules can also feel restrictive, from painting walls to keeping pets.

- Most importantly, renters miss the chance to build long-term wealth through rising home values.

The Decision in 2025: What Should You Do?

Renting makes sense for short-term movers or those seeking flexibility. Buying may still work for stable households in markets where prices are easing. The smart move is to run the numbers locally. In 2025, the choice is less about tradition and more about math and timing. In short, the decision comes down to priorities. Some people care most about monthly cost, while others focus on stability or long-term wealth.

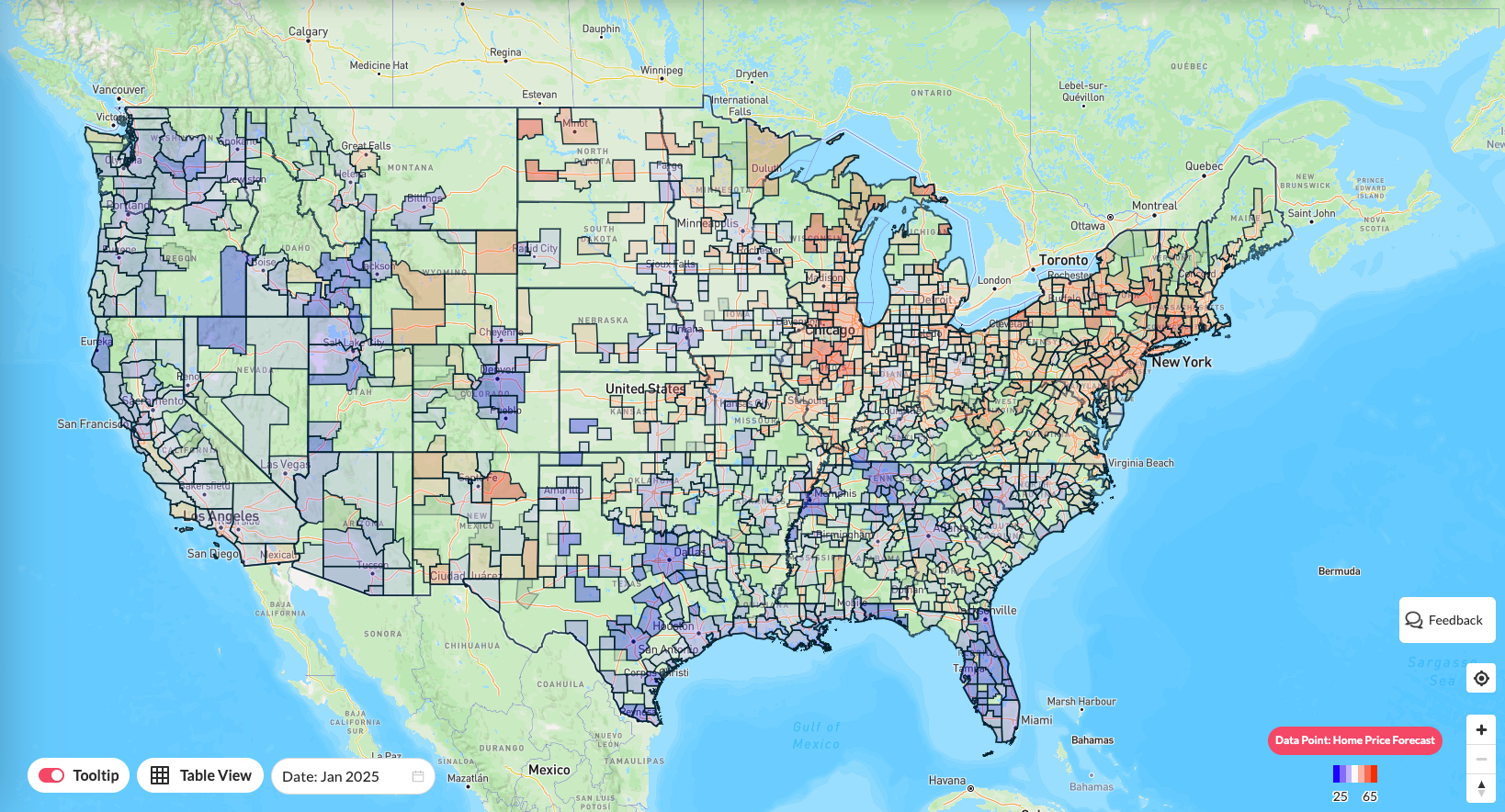

For that, Reventure App provides housing cost insights down to the ZIP code for $39/ month. This helps renters and buyers see which neighborhoods are overpriced and which offer value. It also gives sellers a clearer view of current trends. In today’s cooling but competitive market, localized insight can make the difference between a smart move and a costly mistake.